Download Aggregate Consumption and Production Equilibrium with Sticky Prices and more Schemes and Mind Maps Literature in PDF only on Docsity!

Uncertainty shocks and monetary policy rules

in a small open economy�

Sargam Guptay

ISI, Delhi

This version: 24 November, 2019

Abstract This paper explores the role of exchange rates (both nominal and real) and mone- tary policy in amplifying/ stabilizing the real e ects of global uncertainty shocks in a small open economy. Post global nancial crisis (GFC) of 2008-2009, there has been a surge in the macroeconomics literature on aggregate uncertainty. The recent liter- ature has recognized that global uncertainty shocks reduces private consumption and investment severely in emerging market economies (EMEs). Using data we reproduce stylized facts showing signi cant movements in exchange rates when EMEs are hit with a global uncertainty shock. We nd that interest rate rules are ine ective in stabilizing the exchange rates as well as the domestic economy. With interest rate rules there arises trade-o in in ation and output stabilization. Using a small open economy NK-DSGE model, we show that exchange rate rules (ERRs) reduce welfare losses signi cantly compared to interest rate rules. ERRs also reduce variability of exchange rates, in ation and output remarkably. This occurs because exchange rate rules generate a lower risk premium than interest rate rules. Keywords: Uncertainty shocks; monetary policy; interest rate rules; exchange rate rules; uncovered interest rate parity (UIP), risk premiums JEL Codes: E31, E42, E43, E52, E58, F �I thank Susanto Basu, Chetan Ghate, Morten O. Ravn, seminar participants at the Delhi School of Economics-CDE Seminar (September, 2019), Reserve Bank of India, Mumbai (August, 2019), Conference on Economic Theory and Policy (Ambedkar University, Delhi-March, 2019), 14th^ Annual Conference on Economic Growth and Development (Indian Statistical Institute, Delhi- December, 2018) and 7th^ Delhi Macroeconimcs Workshop (ISI-Delhi, October, 2018) for their extremely helpful comments. This version is a part of conference proceedings, 12th^ International Research Conference (December 2019), Central Bank of Sri Lanka, Colombo. y Corresponding Author: Economics and Planning Unit, Indian Statistical Institute, New Delhi { 110016, India. Tel: 91-11-4149-3942. E-mail: sargamgupta.6@gmail.com.

1 Introduction

There has been a surge in the macroeconomics literature on aggregate uncertainty post global nancial crisis (GFC) of 2008-2009. The role of uncertainty shocks in slowing down the real economy and driving business cycles is getting well recognized in the literature. Using a reduced form VAR, Bloom (2009) estimates that global uncertainty shocks reduce U.S. in- dustrial production by 1 per cent. Gourio et al. (2013) show a similar result for G7 countries. Bloom et al. (2018) show that uncertainty rises sharply during recessions and it reduces GDP by 2.5 per cent. Basu and Bundick (2017); using a new-Keynesian DSGE model, show that demand-determined output is the key mechanism for generating comovements observed in the data as a response to uncertainty uctuations in US. Ravn and Sterk (2017) exposits the role of job uncertainty in amplifying adverse e ect of GFC, using a model featuring labour market with matching frictions and in exible wages. While the literature on the impact of uncertainty shocks on emerging market economies macroeconomic outcomes is less developed, Fern�andez-Villaverde et al. (2011) show adverse real e ects of an increase in real interest rate volatility (uncertainty in real interest rates) on output, consumption and investment. Cespedes and Swallow (2013) argue that global uncer- tainty shocks not only impact consumption and investment demand in advance economies (AEs) but also in emerging market economies (EMEs). Their estimation shows that the impact of such shocks on EMEs is much more severe than AEs. Moreover emerging mar- kets take much longer time to recover due to credit constraints present in these economies. Chatterjee (2018) discusses the role of trade openness in explaining a disproportionately larger real e ects of uncertainty shocks on EMEs compared to AEs, especially during a re- cessionary period.^1 To the best of our knowledge, the role of monetary policy in o setting the adverse e ects of global uncertainty shock in an EME and its link with the exchange rates is not explored in the literature. This paper addresses this gap. We examine the role of exchange rates and monetary policy rules in transmitting the e ect of uncertainty shocks in a small open economy (EME). We observe that exchange rate movements are signi cant in EMEs vis-a-vis AEs, when global uncertainty rises. To be speci c, the data distinctly shows that exchange rates, both nominal as well real, depreciate strongly during periods of high global uncertainty. This happens because capital moves out of EMEs as an immediate response to higher global uncertainty. Typically, when global risks are high investors move their risky asset portfolio into safer assets like US treasury bill and that's why EMEs experience a net portfolio out ow. This is consistent with the (^1) In the trade literature, Magrini et al. (2018) also show that there are ex-ante risks due to trade exposure in Vietnam and these risks a ect consumption growth. An ex-ante shock in the trade literature is closely associated with an uncertainty shock in the macroeconomics literature.

Figure 1 below, when an economy deviates from UIP, the link between nominal interest rates (monetary policy instrument) and the nominal exchange rate breaks down. Thus any attempt to use an interest rate rule to stabilize the economy through the nominal exchange rate is unsuccessful.^6 To summarize, a depreciating domestic currency in EMEs aggravates the contractionary real e ects of an increase in global uncertainty and leads to increase in in ation. Thus, in a small open economy (EME), stabilization of exchange rates is imperative to o set the adverse e ects of increasing global uncertainty, and interest rate rules fail to do so. Finally, we build a small open economy new-Keynesian DSGE model with an uncertainty shock to the world demand and examine the response of real macroeconomic variables under a variety of monetary policy rules. The purpose of this exercise is to look for a monetary policy rule which minimizes the welfare losses since interest rate rules are ine ective here. Singh and Subramanian (2008) have shown that an essential feature that determines the optimal choice of monetary policy instrument is the nature of shocks a ecting the economy. Following this we consider response of the economy under an alternate monetary policy instrument. A most obvious alternate policy to be considered here is a xed exchange rate regime. Cook (2004) has argued that a xed exchange rate regime (PEG) o ers greater stability than an interest rate rule (or exible exchange rate regime) when currency depreciation destabilizes the business cycle. We show that a xed exchange rate regime does only slightly better than an interest rate rule, in terms of welfare losses, as it brings high variability to other nominal variables in the economy like consumer price in ation (CPI), which adjusts more. Although xed exchange rate does bring a greater stability to macroeconomic variables then interest rate rules in the long run. This is di erent from Corsetti et al. (2017), who argues that exible exchange rate regimes perform better then a xed exchange rate regime when the domestic economy faces a negative demand shock (level shock) from abroad. This happens because a exible exchange rate regime stabilizes the demand via depreciation of the domestic currency which a PEG regime does not allow for. This is in contrast to the results we get in this paper for a second moment shock to the demand abroad. The di erence in the results is primarily driven by non-zero risk premiums generated for second moment shocks as UIP does not hold. Since exible exchange rate regimes are associated with higher risk premiums than PEG, the latter performs better under high global uncertainty.^7

high risk premiums. 6

7 This point is also emphasized in Heiperzt et al. (2017): In Corsetti et al. (2017) a depreciation of domestic currency stabilizes demand. This paper looks at two other channels of depreciation which can a ect an economy adversely in the baseline case of exible exchange rates. Firstly when the domestic currency depreciates this increases in ation in the domestic country. Assuming the domestic country is an in ation targeter and is not at the zero lower bound (ZLB)

Figure 1: In presense of global uncertainty shock (a) Monetary policy using nominal interest rates as instrument (left); (b) Monetary policy using nominal exchange rates as instrument (right)

We nd that a monetary policy rule that gives the lowest welfare losses when a small open economy is hit with a global uncertainty shock is an exchange rate rule. When a monetary policy uses the exchange rate as an instrument, the exchange rate follows a rule and is guided by key fundamentals governing the domestic economy, like in ation and output. Since the exchange rate follows a rule and does not oat freely, the hedging motive mentioned above is weakened. Thus, nominal exchange rates are stabilized and welfare losses are reduced signi cantly. Heiperzt et al. (2017) also show that exchange rate rules outperform interest rate rules in a small open economy for shocks to the rst moment. The risk premiums associated with exchange rate rules are also lower, due to a lower hedging motive. The right chart in Figure 1 shows how a link between monetary policy, exchange rates and key real macro variables like in ation and output is restored when exchange rate rules are followed. Exchange rate rules not only reduce welfare losses but also reduce the variability of nominal exchange rates, output and in ation remarkably.

1.1 Empirical evidence

We use a local projection method proposed by Jorda (2005) to look for the e ects of global uncertainty shocks on a wide variety of variables for both AEs and EMEs.^8 To capture global uncertainty we use the VXO index series as proxied in Bloom (2009) and

constraint (the EMEs considered here are not at the ZLB constraint), monetary policy increases the policy rate which has a negative a ect on domestic demand. The second channel is the fall in the investment demand and drying up of the working capital in domestic rms due to depreciation, as discussed in the Introduction to this paper. 8 We use STATA 13 to do our empirical analysis.

0

Percent (^0) Quarters after shock 2 4 6

GDP (EME)

0

Percent (^0) Quarters after shock 2 4 6

GDP (AE)

(a)

0

5

Percent (^0) Quarters after shock 2 4 6

Consumption (EME)

0

5

Percent (^0) Quarters after shock 2 4 6

Consumption (AE)

(b)

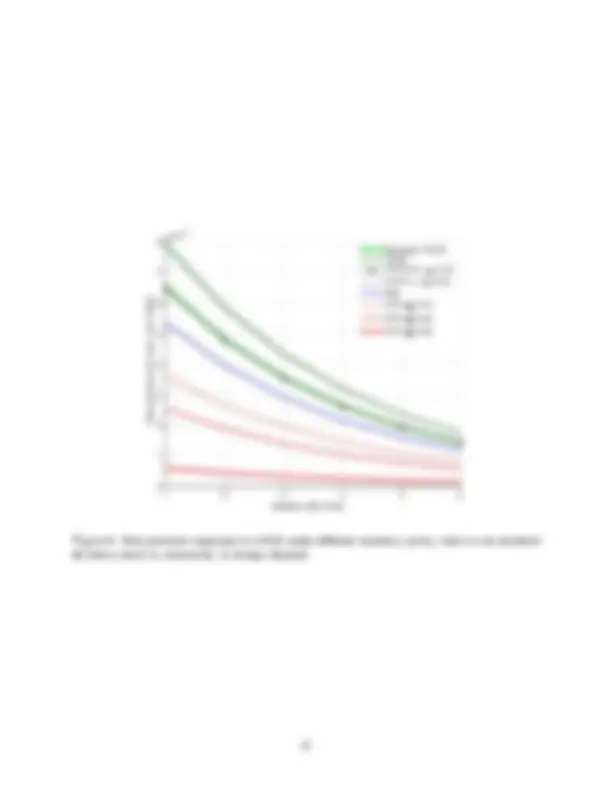

Figure 2: Local projection responses for (a) GDP; (b) Consumption with VXO impulse

in both EMEs and AEs, but the decrease is much higher (upto 10 per cent from the trend) in EMEs compared to AEs. This result is consistent with the empirical facts observed in Cespedes and Swallow (2013): Figure 3a shows capital (net portfolio investment) out ows from EMEs immediately after the shock.^14 About 30 per cent of the capital, as a deviation from the trend, in EMEs ows out when global uncertainty increases. AEs do not experience much change in there capital movement as compared to EMEs. The literature has identi ed high global risk as one of the most important push factor in determining capital out ows from EMEs (see Fratzscher (2012) ; Forbes and Warnock (2012)). As a result of capital out ows, the domestic currency (nominal exchange rate) in EMEs depreciates up to 10 per cent in two quarters after the shock (see Figure 4a). The real e ective exchange rate (REER) also depreciates and remains depreciated up to four quarters after the shock in EMEs (see Figure 4b).^15 No signi cant exchange rate movements are observed in AEs as compared to EMEs. A sustained real or nominal depreciation of the currency ampli es the reduction in real activity and brings instability to the business cycle in EMEs as argued in Korinek (2018) and Cook (2004). The primary reason emphasized in papers mentioned above is the presence of large ex- ternal debt denominated in foreign currency in EMEs. When the currency depreciates, (^14) The series used here is net portfolio investment to GDP ratio. This is done to normalize the series before HP 15 ltering. Since the REER is measure in terms of US dollars, any decrease here indicates real e ective depreciation.

0

20

40 60

80

Percent (^0) Quarters after shock 2 4 6

Net Portf olio investment (EME)

0

20

40 60

80

Percent (^0) Quarters after shock 2 4 6

Net Portf olio investment (AE)

(a)

-^ -^

0

2

4

Percent (^0) Quarters after shock 2 4 6

Trade Balance (EME)

-^ -^

0

2

4

Percent (^0) Quarters after shock 2 4 6

Trade Balance (AE)

(b)

Figure 3: Local projection responses for (a) Net portfolio investment; (b) Trade balance with VXO impulse

balance sheets of rms in EMEs worsens, and this leads to foreign investors pulling out their investments. EMEs also experience a trade de cit in the rst two quarters after a shock before the trade balance starts improving due to currency depreciation (see Figure 3a).^16 Initially, the trade balance falls due to a fall in foreign demand for domestic goods (exports) as consumption in the foreign economy is also low due to higher global uncertainty. Cur- rency depreciation in EMEs leads to a rise in in ation due to a rise in the import good price (see Figure 5a). AEs on the other hand, experience a fall in consumer prices as their aggregate demand falls (see Figure 5b). All countries considered for the present analysis have an in ation targeting mandate with interest rates as a monetary policy instrument. Interest rates thus fall in AEs as a policy response to a contracting economy and de ation (Figure 5a).^17 For EMEs, a contracting economy would suggest reduction in the interest rates (expansionary monetary policy), and an increase in consumer prices with exchange rate depreciation would suggest an increase in the interest rates (contractionary monetary policy). Policymakers in EMEs are thus faced with the trade-o between in ation and the (^16) Series used here is the trade balance to GDP ratio. This is done to normalize the series before HP ltering. 17 Impulse responses for real GDP, real consumption, the trade balance,the real e ective exchange rate, in ation and short term interest rates are strongly signi cant at the 90 per cent con dence level. On the other hand, net portfolio investment and the nominal exchange rate are signi cant nearly at the 80 per cent con dence level. We suspect this happens due to the averaging out e ect in the movement of portfolio investments and exchange rates over a quarter.

output stabilization. Moreover, as the central bank gives more weight to stabilizing in ation in a Taylor type interest rate rule, we observe an increase in the interest rates in EMEs (see Figure 5a).

1.1.1 Summary of stylized facts

The empirical observations explained above can be summarized as following stylized facts: Fact 1: An increase in global uncertainty reduces real activity in both AEs as well as EMEs. EMEs experience a greater fall in GDP and private consumption compared to AEs and also take more time to recover from the shock. Fact 2: An increase in global uncertainty pulls capital (net portfolio investment) out from EMEs. The trade balances deteriorates initially before improving due to an exchange rate depreciation. Fact 3: The capital out ow from EMEs leads to a currency (both nominal and real exchange rates) depreciation. As has been emphasized in the literature, an exchange rate depreciation worsens the balance sheets of rms, which is followed by foreign investors pulling out capital further and thus amplifying the e ect of the shock on the real economy. Fact 4: Consumer prices in EMEs increase due to a depreciation, and monetary policy responds by increasing interest rates. A rise in interest rates can thus reinforce the adverse e ects of global uncertainty shock on the real economy. To explain these facts and understand the role of monetary policy, we build a small open economy NK-DSGE model with uncertainty shocks. The basic framework of the model is adapted from the two country model (foreign and domestic country) discussed in Benigno et al. (2012). While we characterize the domestic economy as a small open econ- omy, the foreign economy is an approximation to the world economy. The uncertainty is present in the preference/ demand shock of households in the foreign economy. We calibrate a small open economy and the world economy to a prototypical EME and AE, respectively.

1.2 Main results

1.2.1 Response to an uncertainty shock to the demand

We nd that the calibration results from the model t well qualitatively with the empirical stylized facts we observe in the data. When a global uncertainty shock hits a SOE, they experience a sudden capital out ow of capital and their nominal exchange rates depreciate. The real e ective exchange rates (REER) also depreciates following a nominal exchange rate depreciation. This result is consistent with stylized Fact 3 we observe in the data. Demand contracts in the economy as agents save more (precautionary savings motive) and consume

less today in a demand determined new-Keynesian model. Net exports rise due to a fall in imports as a result of the depreciation. This result is in line with empirical Facts 1 and 2, although in the data we observe the trade balance improving only after two quarters. Due to a depreciation of the domestic currency, the import prices of foreign goods consumed by domestic households increases. This increases consumer price in ation in the domestic economy. Since the central bank follows a simple Taylor type interest rate rule, the nominal interest rate also rises to stabilize consumer price in ation in the domestic country. This result too qualitatively matches Fact 4 that we observe in the data. The welfare losses in the domestic economy are positive because of adverse real e ects of uncertainty shock. We also nd that the level of price exibility matters for the extent to which uncertainty shock a ect real variables. Under complete price exibility, real variables are not a ected and only nominal variables adjust. This happens because the economy under exible price equilibrium is supply determined and not demand determined. When savings increase due to an uncertainty shock, the supply side of the economy is una ected. Only the price level and the nominal interest rate adjusts here. As a result when savings (in assets) go out of the country, with increasing uncertainty, the price of the asset in domestic country falls. This fall in the asset prices leads to a rise in the nominal rate of interest. Consumer prices also increase to ensure that real savings and real interest rate do not show any change in the new equilibrium.

1.2.2 Role of monetary policy

A positive response of interest rates can reinforce the adverse e ects of uncertainty shocks on the real economy. Moreover, the interest rate response is ine ective in stabilizing exchange rates, both nominal and real, as the UIP breaks down. Further, to examine the role of monetary policy in stabilizing the e ects of a global uncertainty shock, we compare impulse responses from the model under alternate monetary policy rules. We broadly consider two categories of monetary policy rules. The rst category rules are modi ed Taylor type interest rate rules. The second category rules are exchange rate rules. Under exchange rate rules, monetary policy is conducted with exchange rates as a monetary policy instrument. We also consider an extreme case of complete exchange rate stabilization i.e. a xed exchange rate / PEG rule. We nd that welfare losses are lowest in exchange rate rules, followed by a PEG rule. The Taylor type interest rate rules give highest welfare losses. The welfare losses are reduced upto 21 per cent when a central bank switches to following an exchange rate rule from an interest rate rule. Comparing second order moments in long run simulations from the model under di erent rules show a remarkable reduction in the variability of variables when exchange

2.1 Households

The world is assumed to consist of two countries, domestic (D) and foreign (F ) : We assume that domestic economy is a small open economy with size n relative to the world economy, which is modelled as a foreign economy.^20 A continuum of domestic households exist over [0; n], while foreign households from (n; 1]; where n 2 (0; 1) : An agent in each country is both a consumer and a producer, producing a single di erentiated good and consuming all the goods produced in both countries. Also, the population size in each country is set equal to the range of goods produced in that country, such that domestic rms produce goods on [0; n], and foreign rms produce goods on (n; 1]. The preferences of a representative household in domestic country is captured by the following utility function,

E 0

X^1

t=

t (Ct) 1 � �D

1 ��D � !D1 +^ (HD;t �) D

1+�D^!

Here Ct denotes the aggregate consumption index, HD;t denotes hours worked by the repre- sentative domestic household, �D is a measure of the inverse of the intertemporal elasticity of substitution, �D is the inverse of the Frisch elasticity of substitution, and 2 (0; 1) is the discount factor. The aggregate consumption index, Ct, is de ned as,

Ct =

(�D)^1 =�D^ (CD;t)

�D � � 1 D (^) + (1 � �D)^1 =�D^ (CF;t)

�D � � 1 D

� �D�D � 1

where, CD;t and CF;t denotes the consumption index of domestic goods and foreign goods of domestic households, respectively. �D > 0 is the elasticity of substitution between domestic goods and foreign goods for domestic households and �D 2 (0; 1) is the weight given to domestic goods in the aggregate consumption basket, Ct:^21 Analogous to equation (1), the utility function for a representative household in a foreign country is given by,

E 0

X^1

t=

t �F;t^ (C t� ) 1 � �F

1 ��F � !F1 +^ (HF;t �) F

1+�F^!

(^20) We later limit n! 0 to characterize the domestic economy as a small open economy. (^21) When �D > n means a home-bias for domestic goods since the weight given to domestic goods is higher than the size of the country.

where C� t denotes the aggregate consumption index, HF;t denotes hours worked and �F;t is the preference/ demand shock process. The aggregate consumption bundle C t� is given by,

C t� =

(�F )^1 =�F

C D;t�

��F � F� 1

+ (1 � �F )^1 =�F^

C F;t�

��F � F�^1 �^

��F F �^1 (4)

where �F 2 (0; 1) is weight given to domestic goods in the aggregate consumption basket, C t�. Following Benigno et al. (2012); the weights mentioned in the aggregate consumption bundles equations (2) and (4) are related to country sizes through:

1 � �D = (1 � n) � (5) �F = n�: (6)

Here, � 2 (0; 1) is the (common) degree of openness between the domestic and foreign country. When � = 0; there is no trade of either goods or assets happening across the two countries and it represents an autarky case. � = 1, represents a case of complete free trade of both goods and assets between the two countries. Consumption bundles, CD;t, CF;t; C D;t� and C F;t� are Dixit-Stiglitz aggregates of di erentiated goods produced in two countries and are de ned as,

CD;t =

n

� (^) �^1 Z (^) n

0

(CD;t (i)) �� � 1 di

; CF;t =

1 � n

� 1 � Z 1

n

(CF;t (i)) �� � 1 di

C D;t� =

n

� (^) �^1 Z (^) n 0

C D;t� (i)

di

; C F;t� =

1 � n

� 1 � Z 1

n

C F;t� (i)

di

Here � is the elasticity of substitution between the varieties, where a variety is indexed by i 2 [0; 1] :^22 The demand for each variety of a di erentiated domestic and foreign good by each country's household is given as follows,^23

CD;t (i) =

n

PD;t (i) PD;t

CD;t ; CF;t (i) =

1 � n

PF;t (i) PF;t

CF;t (9)

C D;t� (i) =

n

� P �

D;t (i) P (^) D;t�

C D;t� ; C F;t� (i) =

1 � n

� P �

F;t (i) P (^) F;t�

C� F;t (10)

(^22) Note that the elasticity of substitution between the varieties, �; is assumed to be same in both the countries. (^23) Refer to the Technical Appendix 4.2 for derivations.

two countries in terms of domestic prices, and is given by,

Qt = XtP^ t� Pt

Re-writing equation (17) gives us the following relationship between consumer price in ation in the domestic and foreign country,

�� t = �t Qt Qt� 1 �X;t^ :^ (18)

Here, consumer price in ation in the foreign country and domestic country are de ned as �� t = P^ t� P (^) t�� 1 and^ �t^ =^ Pt Pt� 1 , respectively.^ Also, the change in the nominal exchange rate is de ned as, �X;t = (^) XXt�t 1 : The terms of trade is de ned as a ratio of foreign prices to domestic prices, where both price indices are denominated in domestic currency and is given by,

Tt = PF;t PD;t = (^) TTF;t D;t

where we de ne relative price ratios, TD;t = P PD;tt and TF;t = P PF;tt. Using these de nitions of relative price ratios with equation (15), we get the following relation,

TF;t =

1 � �D (TD;t)^1 ��D 1 � �D

# 1 � 1 �D

Similarly, equation (16) can be re-written in terms of gross foreign in ation

�� F;t

; foreign consumer price in ation (�� t ) ; and the terms of trade as,

�� t = �� F;t

�F (Tt)�F^ �^1 + (1 � �F ) �F (Tt� 1 )�F^ �^1 + (1 � �F )

# 1 �^1 �F

where, �� F;t = P^ F;t� P (^) F;t�� 1 :^ For the above described preferences, the total demand for each variety i of the domestic produce is given by,

YD;t (i) = nCD;t (i) + (1 � n) C D;t� (i)

where nCD;t (i) and (1 � n) C D;t� (i) is the aggregate demand of all households in the domestic and foreign country, respectively, for variety i of the domestic produce. Using the demand

functions described in (9) and (10), we get

YD;t (i) =

PD;t (i) PD;t

YD;t (22)

where, aggregate demand for domestic good (all varieties) is given by, YD;t = CD;t+

� 1 �n n

C D;t� : Further, using (13) and (14) in equation (22), we can re-write YD;t in terms of aggregate con- sumption bundles in the two countries, as given by

YD;t = (TD;t)��D

�DCt +

1 � n n

�F Q� t F(TD;t)�D^ ��F^ C t�

Similar to the domestic country, aggregate demand for a variety i of the foreign good is given by,

YF;t (i) =

PF;t (i) PF;t

YF;t (24)

where, aggregate demand for the foreign good (all varieties), YF;t = (^) (1�nn) CF;t + C F;t� : Aggre- gate demand, YF;t; can be re-written in terms of aggregate consumption bundles in the two countries as,

YF;t = (TF;t)��D

� (^) n (1 � n) (1^ �^ �D)^ Ct^ + (1^ �^ �F^ )^ Q

�F t (TF;t)�D^ ��F^ C t�

Households in the domestic and foreign country maximize (1) and (3) subject to the following ow budget constraints,

WD;tHD;t + $D;t � PtCt � BD;t + Et fBD;t+1Mt;t+1g ; (26) WF;tHF;t + $F;t � P (^) t� C t� � BF;t + Et

BF;t+1M (^) t;t�+1 (27)

respectively. Here WD;t and WF;t are nominal wages in the domestic and foreign country, respectively. The nominal wages are decided in a common labour market in each country. Also, $D;t and $F;t are the nominal pro ts which households receive from owning monopo- listically competitive rms in the domestic and foreign country, respectively. Each household in each country holds equal shares in all rms and there is no trade in rm shares. The asset markets are assumed to be complete both at domestic and at international levels. House- holds trade in state-contingent nominal securities denominated in the domestic currency. BD;t+1 is the state-contingent payo at time t + 1 of a portfolio of state-contingent nominal securities held by a household in the domestic country at the end of period t. The value of this portfolio can be written as Et fBD;t+1Mt;t+1g ; where Mt;t+1 is the nominal stochastic

Here �D;t and �F;t are Lagrangian multipliers for domestic and foreign country households, respectively. Combining the Euler equation from equation (29) and (30) with equation (28) ; we get the following complete asset market condition,

Qt+1 = � Et

�F;t+1C t��+1�F Et

C t�+1�D

where, � = Q 0 C 0 ��D �F; 0 C�� 0 �F^ is the ratio of marginal utilities of nominal income across countries in the initial period. Equation (28) when combined with de nitions of nominal stochastic discount factors i.e. Et fMt;t+1g = (^) (1+^1 Rt) and Et

M (^) t;t�+1 = (^) (1+^1 R� t ) ; gives the following uncovered interest rate parity (U IP ) condition (log-linearized),

rt � r� t = Et f�et+1g (35)

where, rt; r� t and Et f�et+1g are logs of (1 + Rt) ; (1 + R� t ) and Et

nX Xt+ t

o ; respectively. Following Menkho et al. (2012), Backus et al. (2010) and Benigno et al. (2012), we de ne time-varying risk premiums as deviations from the UIP condition, mentioned in equation (35) : The log-linearized time-varying risk premiums, rpt; are excess returns on holding do- mestic currency and written as follows,

rpt = rt � r� t � Et f�xt+1g : (36)

2.2 Firms

The domestic country produces goods on the interval [0; n] and the foreign country on (n; 1]: A rm producing variety i of a good in the domestic and foreign country follows a production function linear in labour, given by,

YD;t (i) = AD;tHD;t (i) (37) YF;t (i) = AF;tHF;t (i) ; (38)

respectively. Here, AD;t and AF;t are the productivity levels (common) following exogenous processes. HD;t (i) and HF;t (i) are composites of all the di erentiated labour supplied by household h in each country, as given by,

HD;t (i) =^1 n

Z (^) n 0

HD;th (i) dh ; HF;t (i) = (^1) �^1 n

Z 1

n

HF;th (i) dh (39)

where HD;th (i) and HF;th (i) are the labour supplied by household h to rm i in the domestic and foreign country, respectively.

2.2.1 Price setting

In the benchmark model we assume that rms in both the countries have nominal price rigidities in the form of price stickiness. We follow Calvo (1983) to capture price stickiness here. In each period only (1 � (^) D) fraction of rms in the domestic country can reset their prices independent of whether they had a chance to reset them in the last period. A rm i which gets a chance to reset its prices, P (^) D;t(i); maximizes a discounted sum of current and future expected values of pro t, given by

max P (^) D;t(i)

X^1

k=

kDMt;t+k^ �P (^) D;t(i)YD;t+k (i) � M CD;t+kYD;t+k (i)�^ (40)

where M CD;t+k is the nominal marginal cost of domestic rms in period t + k and is the same for all rms as the nominal wage is decided in a common labour market and all rms face a common productivity level realization. The demand function YD;t+k(i); for each rm i in period t + k is given by,

YD;t+k(i) =

P (^) D;t(i) PD;t+k

YD;t+k

The optimal price chosen by rms re-setting prices is given by,

P (^) D;t(i) = � � � 1

P^1

k=

kDMt;t+kM CD;t+kYD;t+k(i) P^1 k=

kDMt;t+kYD;t+k(i)

where (^) ��� 1 is the constant markup charged by rms. As can be seen from equation (41) ; the optimal price today depends on not just current but future marginal costs, and also demand conditions in the economy. A rm i, which does not reset its price is assumed to keep the prices same as last year's prices, PD;t� 1 (i): Thus, the law of motion for the aggregate producers price index (PPI) in the domestic country for Calvo's model can be written as,

PD;t =

h D (PD;t� 1 )^1 ��^ + (1^ �^ D)^

P (^) D;t

� 1 ��i^1 �^1 � : (42)