Theory of Production

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

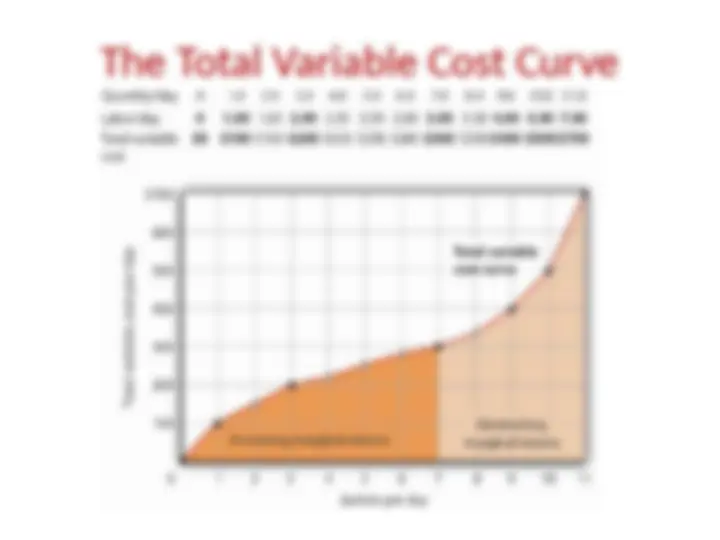

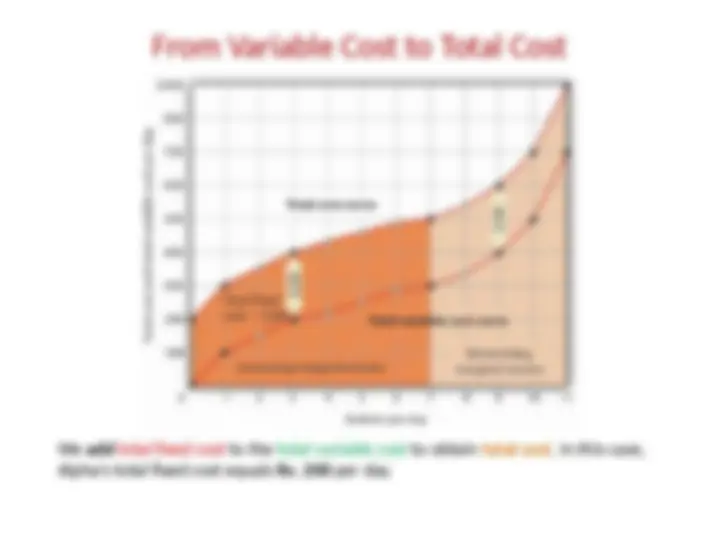

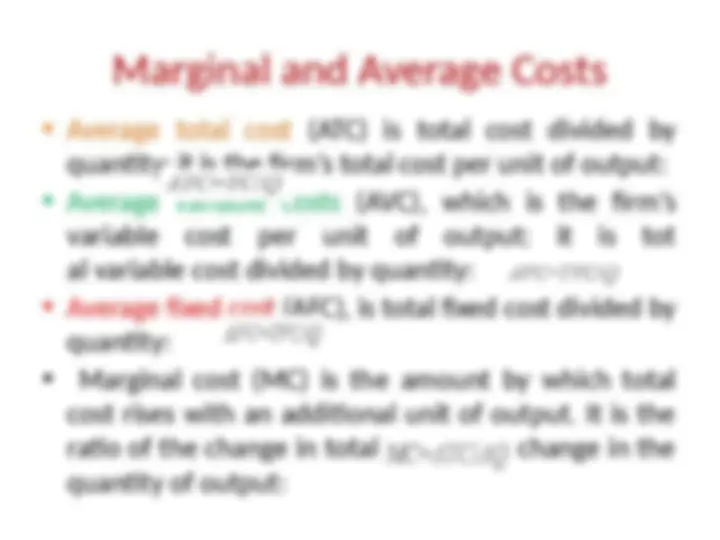

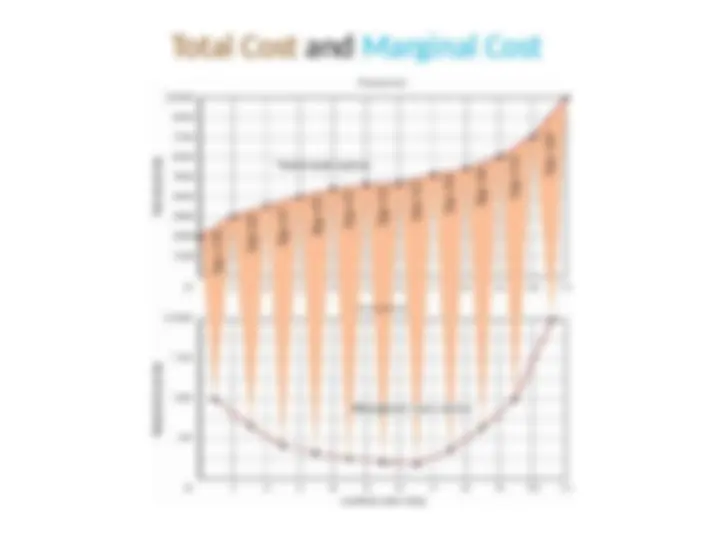

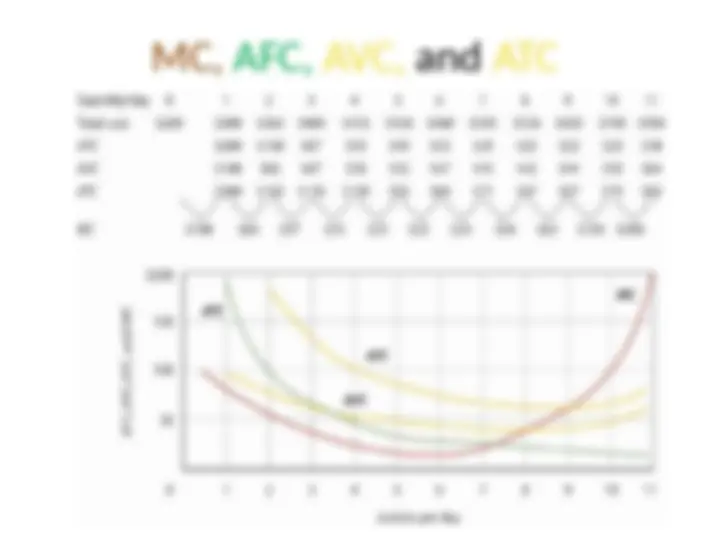

The basic concepts of production theory, including inputs, fixed and variable inputs, short and long run, and the method of production. It also covers the production function, short-run production function, total product curve, total cost, total fixed cost, total variable cost, marginal and average costs, and the relationship between them. graphs and examples to illustrate the concepts.

Typology: Schemes and Mind Maps

1 / 34

This page cannot be seen from the preview

Don't miss anything!

Basic Concepts of Production Theory

Basic Concepts of Production Theory

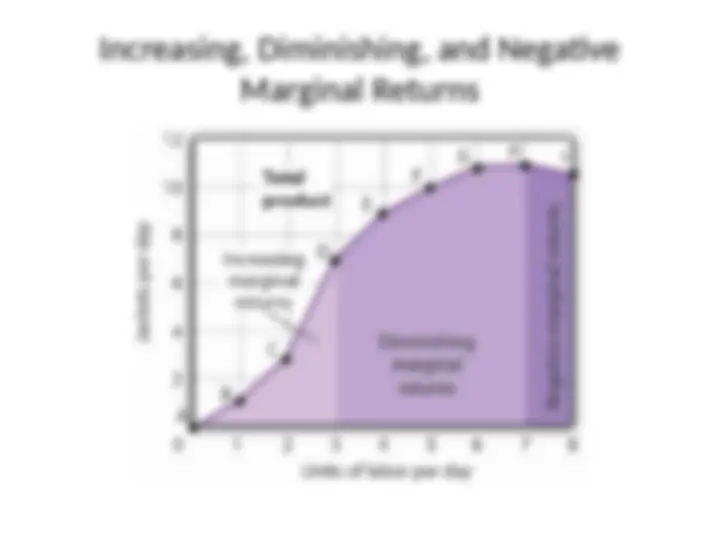

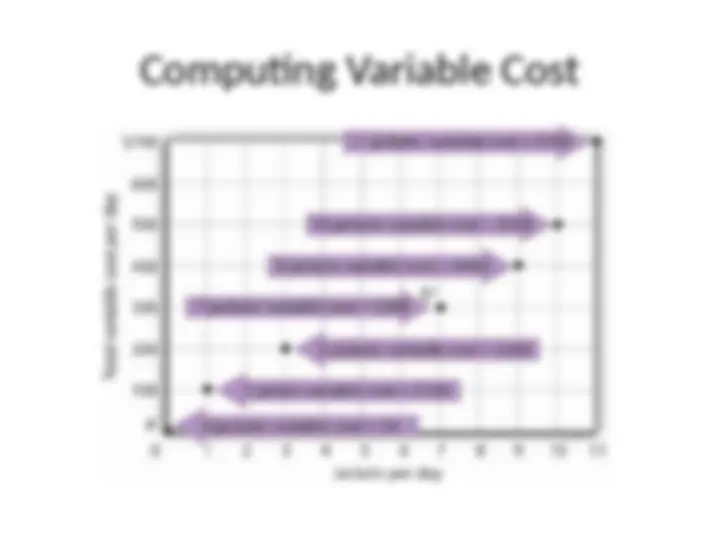

Total Product Curve (TP) A total product (TP) curve shows the quantities of output that can be obtained from different amounts of a variable factor of production, assuming other factors of production are held constant.

From Total Product to the Average and Marginal Product of Labor