Download The Evolution and Importance of Management Accounting and Controlling and more Study Guides, Projects, Research Accounting in PDF only on Docsity!

Lund University School of Economics and Management

Department of Business Administration BUSN68 Master Degree Project

Spring 2016

The role of management accountants

A study of contextual factors and changes in the role over time

Master’s Programme in Accounting and Management Control

Authors:

Anna Trubchik & Ina Rudelsberger

Supervisor:

Anders Anell

i

Abstract

Seminar date 30 May 2016 Course BUSN68^ –^ Degree Project: Accounting and Management Control Authors Anna Trubchik and Ina Rudelsberger Advisor Anders Anell Five key words Controller, Management accountant, Role, Contextual factors, Requirements Purpose The aim of the thesis is to analyse the current role of management accountants, how it is affected by contextual factors, and how it has changed over time. Methodology A^ quantitative^ content^ analysis^ of^ job^ advertisements^ is conducted. The factors of analysis are identified based on a combination of deductive and inductive approach. Theoretical perspectives Based on a literature review on the role of management accountants, its change over time, and the contextual factors influencing the role and the design of MCSs, a theoretical framework of the most important contextual factors and requirements in management accountants is developed. It is further adjusted to incorporate additional factors identified to be relevant through the empirical analysis. Empirical foundation The sample consists of job advertisements for Germany and the UK, which are collected on the websites indeed.de and indeed.co.uk respectively. Information about the companies is additionally collected through further available online resources. Conclusions First,^ reporting,^ planning,^ budgeting,^ forecasting,^ cost accounting, MS Office and MS Excel, ERP and SAP knowledge as well as communication, analytical and teamwork skills are found among the most important requirements in management accountants and controllers today. Second, the results indicate that the country of origin, size, matureness and geographical scope are the most influential contextual factors regarding the role of management accountants within the examined sample. Finally, a conclusion about the change and enhancement of management accountants’ role towards a business partner can be made.

iii

vi

- 1 Introduction Table of content

- 1.1 Background

- 1.2 Research purpose and questions

- 1.3 Outline of the thesis

- 2 Methodology

- 2.1 Choice of the research approach

- 2.2 Description of the chosen method

- 2.3 Avoidance of subjectivity

- 2.4 Justification of the chosen search engine

- 2.5 Sample choice....................................................................................................

- 2.6 Limitations of the method

- 3 Literature review

- 3.1 Management accounting..................................................................................

- Definition and development of the concept...............................................

- Contextual factors influencing MCSs

- 3.2 The role of management accountants

- Definition and title of the position.............................................................

- Position of the management accountant in the hierarchy

- Changing role of management accountants

- Factors influencing the role of management accountants

- 3.3 Tasks and requirements

- Tasks performed by management accountants

- Requirements in management accountants

- 4 Development of a theoretical framework

- 4.1 Choice of contextual factors to be analysed

- 4.2 Choice of requirements to be analysed............................................................

- 5 Results

- 5.1 Adjusted framework for the analysis...............................................................

- 5.2 Presentation of the sample

- 5.3 The role of controllers as described in job advertisements

- 5.4 Influence of the examined contextual factors on the role of controllers

- Country of origin

- Size

- Matureness

- Listing on the stock exchange

- Geographical scope

- Type and industry

- 6 Discussion iv - time 6.1 The role of controllers as described in job advertisements and its changes over - Education and work experience - Professional requirements - Personality requirements - Summary....................................................................................................

- 6.2 Influence of the examined contextual factors on the role of controllers - Country of origin - Size - Matureness - Listing on the stock exchange - Geographical scope - Type and industry - Summary....................................................................................................

- 6.3 Contribution and implications for practitioners - Contributions - Implications for practitioners

- 6.4 Limitations and possible directions for future research

- 7 Summary and conclusion

- Appendix A: Developed framework for the analysis

- Appendix B: Description of possible manifestations and assumptions

- Appendix C: Example of an advertisement being processed

- Appendix D: Distribution of British education requirements (professional training)

- Appendix E: Subject and focus specified in German education requirements

- Appendix F: Direction of influence of the examined contextual factors

- Appendix G: Comparison of the results with previous studies

- Appendix H: Comparison of Germany and the UK by cultural dimensions

- References

- Table 2.1 Inclusion and exclusion criteria List of tables

- Table 3.1 Evolution of the scope of controlling

- Table 3.2 Definitions of management accounting and controlling

- Table 3.3 Definitions of management accountant and controller

- Table 3.4 Summary of the requirements in management accountants

- Table 4.1 Summary of the contextual factors taken for the analysis based on the literature

- Table 4.2 Summary of the requirements taken for the analysis based on the literature

- Table 5.1 Summary of the sample characteristics

- Table 5.2 Professional training requirements in the UK

- Table 6.1 Overview of the studies considered for comparison

- Table 6.2 Summary of the comparison with previous studies

- Figure 1.1 Outline of the thesis List of figures

- Figure 3.1 The controller's four roles

- Figure 3.2 Possible organization of the controller function

- Figure 3.3 Controller roles and group strategies

- Figure 3.4 Controller roles and business strategies

- Figure 3.5 Controller roles and economic cycles

- Figure 3.6 Classification of requirements

- Figure 5.1 Education requirements

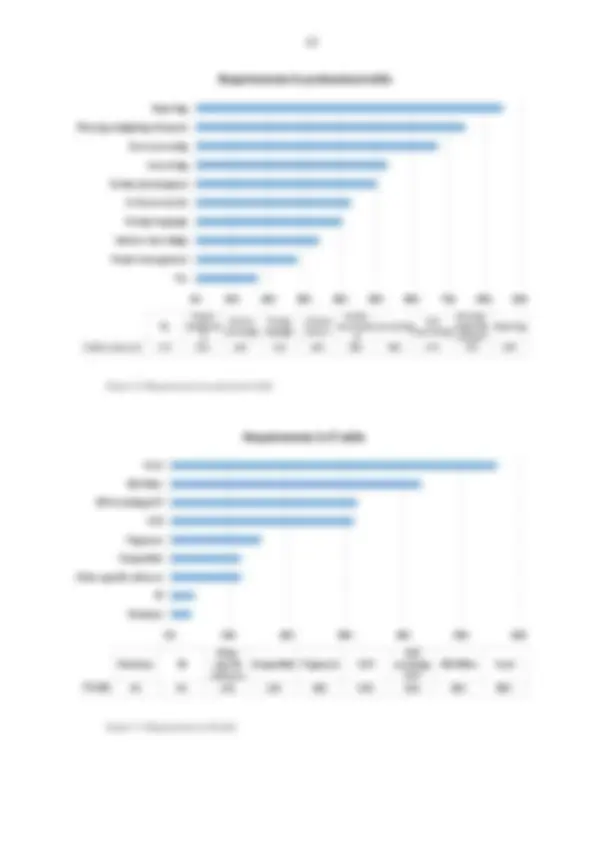

- Figure 5.2 Requirements in professional skills

- Figure 5.3 Requirements in IT skills

- Figure 5.4 Requirements in personality criteria

- Figure 5.5 Education requirements by country

- Figure 5.6 Requirements in professional skills by country

- Figure 5.7 Requirements in IT skills by country

- Figure 5.8 Requirements in personality criteria by country

- Figure 5.9 Distribution of the sample by size

- Figure 5.10 Requirements in professional skills influenced by size

- Figure 5.11 Requirements in IT skills influenced by size

- Figure 5.12 Requirements in personality criteria influenced by size

- Figure 5.13 Requirements in professional skills in relation to companies’ matureness

- Figure 5.14 Requirements in IT skills in relation to companies’ matureness

- Figure 5.15 Requirements in personality criteria in relation to companies’ matureness

- Figure 5.16 Requirements in IT skills in relation to the listing status

- Figure 5.17 Requirements in professional skills in relation to geographical scope

- Figure 5.18 Requirements in IT skills in relation to geographical scope

- Figure 5.19 Requirements in personality criteria in relation to geographical scope

- Figure 5.20 Requirements in professional skills in relation to companies’ type

- Figure 5.21 Requirements in IT skills in relation to companies’ type

- Figure 5.22 Requirements in personality criteria in relation to companies’ type

- Figure 6.1 Development of controlling tools over time

vii

List of abbreviations

AAT Association of Accounting Technicians

ACA Associate Chartered Accountant

ACCA Association of Chartered Certified Accountants

BI Business Intelligence

CA Chartered Accountant

CCAB Consultative Committee of Accountancy Bodies

CEO Chief Executive Officer

CFO Chief Financial Officer

CIMA Chartered Institute of Management Accountants

ERP Enterprise Resource Planning

ICAEW Institute of Chartered Accountants in England and Wales

ICB Industry Classification Benchmark

ICV Internationaler Controller Verein

IMA Institute of Management Accountants

IT Information Technology

MCS Management Control System

MNC Multinational Corporation

the example of Germany and the UK as well as several company characteristics. Finally, it will be analysed, to what extent and how the role has changed over time by comparing the results to previous empirical studies.

This leads to the formulation of three research questions: What are the role of management accountants and the requirements in them? How is the role of management accountants influenced by contextual factors? How has the role of management accountants changed over time? 1.3 Outline of the thesis The remainder of the thesis is structured as follows:

Figure 1.1 Outline of the thesis Chapter 2 – Methodology In this chapter, the chosen method is described and justified. Some limitations are pointed out and the efforts taken to avoid subjectivity are discussed. Furthermore, the selection of the sample is outlined.

Chapter 3 – Literature review This chapter starts with a literature review on management accounting, consisting of its development, the most important contextual factors affecting the design of MCSs and some limitations of these factors. Afterwards, the role of management accountants is examined more closely. The title of management accountants, their position within a company’s hierarchy, their changing role and finally a discussion of the factors influencing their role is described. Afterwards, the tasks performed by management accountants and the requirements in them are presented.

Chapter 4 – Development of a theoretical framework The chapter discloses the development of a theoretical framework of the contextual factors, tasks and requirements based on the conducted literature review. This framework constitutes the basis for the further empirical analysis.

Methodology Literature review^ Theoretical framework Results Discussion^ Summary & conclusion

Chapter 5 - Results To begin with, the theoretical framework is adapted according to the inductively identified additional contextual factors and requirements. Then, the results of the empirical analysis are presented. First, an overall overview of the sample is given. Then, the role of management accountants, as described in the advertisements, is presented. After that, the impact of the contextual factors on the role is described.

Chapter 6 - Discussion The chapter starts with a discussion of the role of management accountants as well as its changes over time. Then, an elaboration on the impact of the contextual factors on the role follows. Thereafter, the contributions to the research landscape as well as the implications for practitioners are described. Finally, the limitations of this thesis and areas for future research are outlined.

Chapter 7 – Summary and Conclusion The paper concludes with summing up the conducted analysis including the most important results, explanations and conclusions.

mentioned requirements in characteristics and skills (Rabinowitz & Fawcett, n.d.). A visualised numerical presentation of the results allows not only to describe the observed requirements and their relations to contextual factors, but also to visualize the importance of particular aspects. Thus, a quantitative content analysis of job advertisements was considered advantageous.

The next decision concerned the kind of job advertisements – whether printed or online. Online advertisements were chosen for several reasons. One advantage is that they are easier to obtain compared to printed ones. However, the more important reasons are that they allow the search for key words, which simplifies the assessment, as the relevant ads can easily be filtered. That avoids a time-consuming search for relevant ads (France, 2010). Furthermore, the online search for job applicants is getting increasingly common (Curry, 2000; Jansen, Jansen & Spink, 2005; Johnson, 2003). Bruce (2004) also states that companies of all sizes use online recruitment as well as that it is used for jobs of all hierarchical levels. Therefore, there is no danger of the data being biased in that respect. In addition, Berens et al. (2013) argue that online advertisements may even provide a more comprehensive picture as companies advertise not only core positions, but also less important jobs online. Furthermore, employers have no space limitations in their online advertisements as is the case with print media. That allows them to specify all criteria considered relevant and to avoid having to focus on only very few important ones (Berens et al. 2013).

Finally, in order to analyse how tasks and requirements in skills and knowledge of management accountants have changed over time, the results of this study were compared to the previous research in the area. Here, the focus was set on studies with the same approach of analysing job advertisements as only this allows for a direct comparison of changes in the percentages over time whereas the resulting percentages of, for example, a survey, will naturally differ and are therefore only of limited suitability for the comparison. However, such studies had to be taken into consideration as well to compare the relative importance and development over time and due to the lack of more appropriate comparison material for the UK for many of the analysed requirements.

2.2 Description of the chosen method First, a literature review was conducted to determine contextual factors affecting the role of management accountants and requirements in them. Afterwards, the most important and suitable ones for the empirical analysis were summed up in a theoretical framework. The review also revealed the key words to find relevant job advertisements. For the UK, the term “management accountant” was used while for Germany “controller” was the key word. The word “controller” was also seen as the closest translation of the term “management accountant” from German into English. Thus, to ensure better comparability, these key words have been applied.

For each factor of analysis, the possible manifestations were then defined. For example, the experience requirement was assigned the possible expressions “no experience required”, “one year”, “several years” and “time unspecified”. For requirements in personality criteria, manifestations such as “communication”, “teamwork”, and “interpersonal skills” were included. In order to see whether they were suitable or if revisions were necessary, a sample analysis of 20 advertisements was conducted – half of them German and the other half British. In other words, the applicability of the chosen approach was tested on a small pilot sample. During this analysis, it was additionally considered whether there were any requirements and tasks frequently demanded which were not part of the originally examined ones. These were then added and the framework for the analysis was adjusted accordingly. However, the goal of this paper is not to provide a full list of all possible requirements and tasks that companies might expect from their future employees, but rather to focus on the most important ones and to see the relations to contextual factors and to define the contemporary role of management accountants. Therefore, less often mentioned characteristics were omitted to avoid a too long list of factors. Furthermore, we analysed part of the employment advertisements independently from each other to ensure a coherent and unbiased categorization (Weber, 1990). Differences and problems were discussed and a consistent procedure agreed on. For example, one issue that occurred was how to treat characteristics not being required, but only desired. In the end, it was decided that a distinction would be too detailed and there was no obvious reason which value a separation could add. Thus, they were treated like strict requirements. That is in line with previous research (Berens et al. 2013). Then, the analysis of the remaining advertisements followed. After the analysis, randomly selected ads were analysed again and compared to the previous categorization results. This is supposed to help ensure accuracy and reliability (Weber, 1990) and revealed no differences compared to the initial categorization.

2.3 Avoidance of subjectivity When researchers are aware of previous literature and have expectations about the results of their study, there is always a danger of the results being biased towards these previous findings, as they may unconsciously interpret the data accordingly. Thus, there may be a certain level of subjectivity involved (Mauthner & Doucet, 2003; Peshkin, 1998; Ratner, 2002). In addition, we might have a possible subjective impact on the analysis as it was necessary to apply our own knowledge on the categorization. This knowledge differs among different people and is influenced by various factors such as culture. Thus, this may have an effect on the analysis (Cicourel, 1964, cited in Bryman & Bell, 2015; Garfinkel, 1967, cited in Bryman & Bell, 2015). To avoid the risk of subjectivity, different measures were taken. First, the analysis was conducted blindly. That means that the company characteristics were only collected and added after all advertisements were analysed so that

A broad variety of different job meta search engines exists. There are more than 15 different ones both in Germany (Berufsstrategie, n.d.; Der große Jobbörsen-Vergleich, 2013; Sicking, 2013) and the UK (Alexander Chase, n.d.; Jobs4, n.d.; Undercoverrecruiter, n.d.). The decision criteria to choose the most suitable search engine were popularity, volume and being available in both countries. It was considered advantageous to choose a provider covering both Germany and the UK as this would ensure that the same search algorithm would be applied to the whole sample. That avoids possible biases that could have been an issue otherwise. This last criterion reduced the choice to CareerJet, Indeed, jobrapido and JobRobot (Der große Jobbörsen-Vergleich, 2013; jobs4, n.d.; Undercoverrecruiter, n.d.). Their ratings are inconsistent, but Indeed and jobrapido were always among the top seven (Adams, 2012; Der große Jobbörsen-Vergleich, 2013; Robert Half, n.d.; ServiceValue, 2015; Sicking, 2013) and Doyle (2016) and Miller-Merrell (2015) consider it to be the best one. Comparing them by size shows that Indeed is the biggest one. Therefore, the choice was made in favour of Indeed.

2.5 Sample choice The chosen meta search engine provided a large number of job advertisements. The search was specified so that the job ads needed to include the terms “controller” in Germany and “management accountant” in the UK directly in the title of the ad. The search, which was conducted on 16 April 2016 for Germany and on 18 April 2016 for the UK, revealed a number of 3 167 and 3 270 job advertisements respectively. It was clear that the analysis of all ads would be too far going. However, the true number of results is smaller than that as they include redundant as well as irrelevant ones. For example, one of the German ads was looking for a developer for 32bit microcontrollers and was immediately omitted.

Furthermore, all job advertisements recruiting applicants for internships were excluded as they were expected to differ significantly from the other ads and not to display the true requirements in controllers as internships are usually still absolved during the education. Trainee positions were excluded as well as their number was very low so that conclusions regarding them would not have been possible, but still, they might differ from ordinary jobs. Moreover, those advertisements, for which it was not possible to obtain the required data were omitted. This was mostly the case for jobs advertised by staffing agencies as they usually do not reveal the name of the employer so that company related factors such as size and matureness could not be determined. Especially in the UK, a high percentage of the advertisements was posted by staffing agencies. For some companies, the later analysis also showed that it was not possible to obtain all supplementary information. In these cases, the companies were contacted by e-mail. If they failed to provide the information within three days, they were excluded from the sample as well. As mentioned before, all advertisements that appeared more than one time were also excluded. An overview of the inclusion and exclusion criteria is presented in Table 2.1.

Inclusion criteria Country Germany UK Key word Controller Management accountant Time Availability on 16 April 2016 Availability on 18 April 2016

Exclusion criteria Internship Trainee programme Company name not specified Redundancy Impossibility to obtain all necessary company related information Table 2.1 Inclusion and exclusion criteria Previous studies following a similar approach as we do, had analysed 116 and 189 job advertisements respectively (Bramsemann, 1978; Gruber, 2015). Thus, in order to keep up with them, we aimed for a final sample size of 200 advertisements with equal German and British representation of ads. In addition, we took into account the possibility that a number of ads might not be useful. Thus, the search results were sorted by relevance and the first 170 advertisements for each country fulfilling the immediately assessable criteria were saved. Saving them offline was supposed to ensure their availability throughout the analysis period and for review if this was found to be necessary at a later point of time. During the analysis, a number of these advertisements were then excluded and reduced to 100 for each country, following the exclusion criteria.

2.6 Limitations of the method The applied research approach may be subject to some limitations. First, the question of representativeness should be kept in mind, as our study is based on a limited number of advertisements, considers only those being published on the internet and is restricted to Germany and the UK. Second, the advertisements themselves might contain several deficiencies. They might not be updated sufficiently by the companies and be influenced by advertisements of other companies. Furthermore, the analysis possibilities are limited by the information provided in the ads. In addition, the amount of data available through the ads might differ and be incomplete in some cases. That might limit the representativeness of the sample and generalization of the obtained results. Further, the ability to measure certain contextual factors is restricted with the chosen approach as deeper knowledge of the companies is required to determine several of them. What is more, certain aspects of the applied search algorithm might influence the composition of the sample, making it biased towards a particular type of companies included in the analysis. Moreover, as our analysis is limited to a certain key date, the comparability over time regarding the changes in requirements is only feasible by comparing the results with previous studies, which limits the comparability possibilities.

on standardization of processes and, as a result, such tools as standard costing and overheads allocation through labour costs have been developed. The 20th^ century brought new changes of the environment and new challenges for management accounting to handle. Thus, the growth of corporations required new techniques for analysis and, during that time, ROI, budgeting and forecasting have been suggested as solutions. Towards the end of the 20th^ century, Johnson and Kaplan (1987) accused management accounting of having lost its relevance. This period in management accounting is marked with changes towards a more strategic focus and appearance of a variety of new techniques such as the Balanced Scorecard and Activity Based Costing (Marchant, 2013).

Roman, Roman and Meier (2014) also provide a brief summary of the core concepts of controlling for the last decades:

controlling as an administrative record tracking (the ’80s) controlling as an administrative information system (end of the ’80s); controlling as planning and control (beginning of the ’90s); controlling as coordination activity (the ’90s); controlling as business administration (end of the ’90s); controlling as a system for coordinating decision-making process (the 2000s) (Roman, Roman & Meier, 2014, p.49). Thus, it can be observed that management accounting has overcome decades of changes embracing changes in the environment and variations across companies following these changes. Therefore, it is not surprising that different definitions of management accounting can be found in the literature. Table 3.2 presents a selection of them.

It can be stated, that the main purpose and function of management accounting can already be derived from the definitions presented above. Hence, providing information appears to be one of the most important purposes and functions.

In addition, Roman, Roman and Meier (2014) explicitly define the purpose and objective of controlling within the organization. According to the authors, the arrangement of the stand-alone components such as the information or planning and control system, as well as the verification of their utility and bringing them together in a system constitutes the main purpose of controlling. Furthermore, Roman, Roman and Meier (2014) see the enhancement of transparency as a main objective of controlling.

Source Definition Morse, Davis & Hartgraves (1984, p.17)

“Management accounting is concerned with providing financial information to persons inside the organization, especially managers.” Horngren & Foster (1987, cited in Nilsson, Olve & Parment, 2011, p.52)

“Management accounting is the identification, measurement, accumulation, analysis, preparation, interpretation, and communication of information that assists executives in fulfilling organizational objectives.” Horngren, Bhimani, Datar & Foster (2002, p.6)

“Management accounting measures and reports financial information as well as other types of information that are intended primarily to assist managers in fulfilling the goals of the organization.” Horngren, Sundem, Stratton, Burgstahler & Schatzberg (2011, p.G12)

“The branch of accounting that produces information for managers within an organization. It is the process of identifying, measuring, accumulating, analysing, preparing, interpreting, and communicating information that helps managers fulfil organizational objectives.”

Nilsson, Olve & Parment (2011, p.14)

“Management control consists of formalized information-based routines, structures and processes which management uses to formulate and implement strategies by influencing behaviour within the organisation.” Roman, Roman & Meier (2014, p.47)

“Controlling is a functional management concept with the role of coordinating the planning, the control and the information towards the desired end-result.” Pavlovska & Kuzmina- Merlino (2015, p.31)

“Management system which provides flexible planning for dynamic targets, and provide proactions for unpredictable events.”

CIMA (n.d.-b)

“Management accounting combines accounting, finance and management with the leading edge techniques needed to drive successful businesses.” Table 3.2 Definitions of management accounting and controlling Turning to the functions of management accounting, the following list can be constructed according to Kumar (2011): planning and forecasting, modification of data, interpretation, management control and communication. Sharma (2015) emphasizes planning, organizing, controlling and decision-making among the most important functions of management accounting. Based on the “skillset” of its members identified by the CIMA (n.d.-b), the functions of planning, information analysis for decision-making, formulation of business strategies, risk identification and management as well as communication can be considered of utmost importance.

As it can be observed from the development disclosed above, management accounting is significantly influenced by changes in the environment and the corresponding development of companies. Thus, it can be assumed that the context plays an important role in designing the MCS of a particular company. Consequently, based on this, the system might vary across companies.