Download Understanding the Cash Flow Cycle and Working Capital Management and more Slides Finance in PDF only on Docsity!

The Cash Flow Cycle

Cash and Net Working Capital

• The cash flow cycle – where cash comes from…how it is used to

finance the operations of the firm…and how it is recovered and

how it grows over time is a crucially-important part of

understanding how a business functions.

Cash and Net Working Capital

Activities that Decrease Cash

• Decreasing long-term debt

• Decreasing equity

• Decreasing current liabilities

• Increasing current assets other than cash

• Increasing fixed assets

• Paying dividends

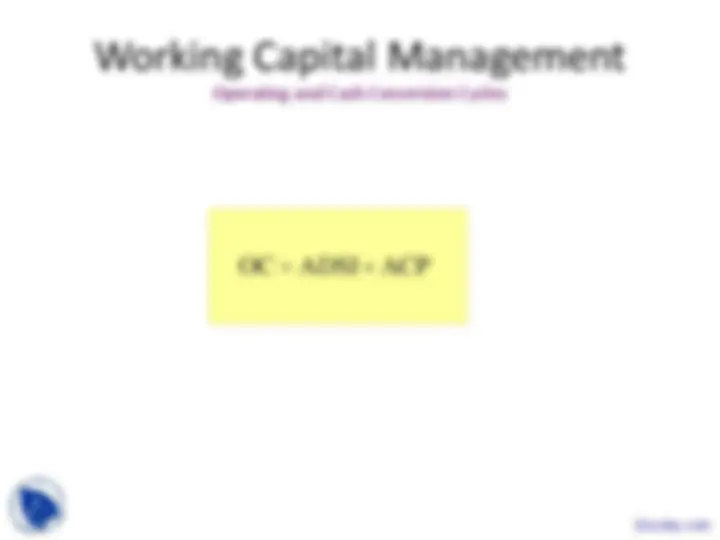

Operating Cycle

Operating cycle is the time period

between the acquisition of inventory and

when cash is collected from receivables.

Example of Exhaustion of the Liquid Resources of a

New Firm

A simple example of a $1.0 million equity investment in

a business levering additional financial resources

and the need to finance the growth of the

business leaving it exhausted of cash resources.

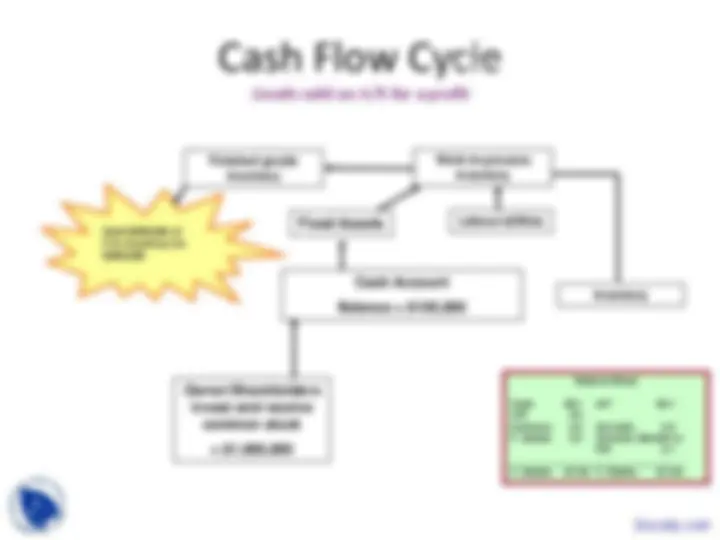

Cash Flow Cycle

Start

Cash Account

Balance = $

The entrepreneur opens a

current account in the name of

the business. Step 1

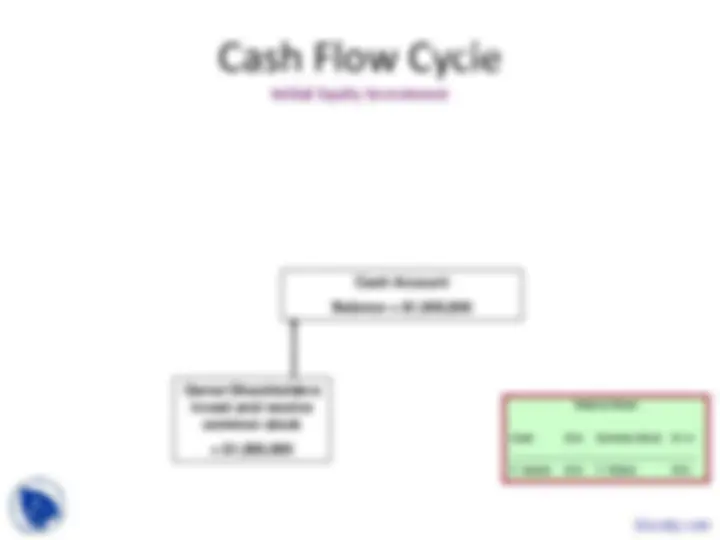

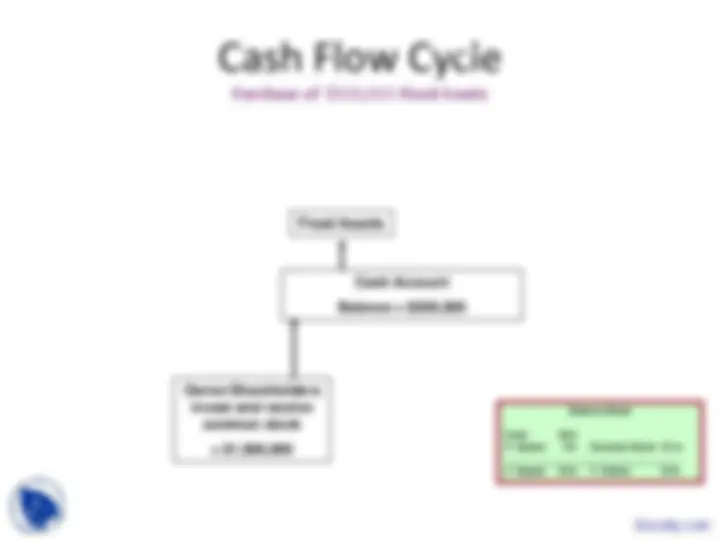

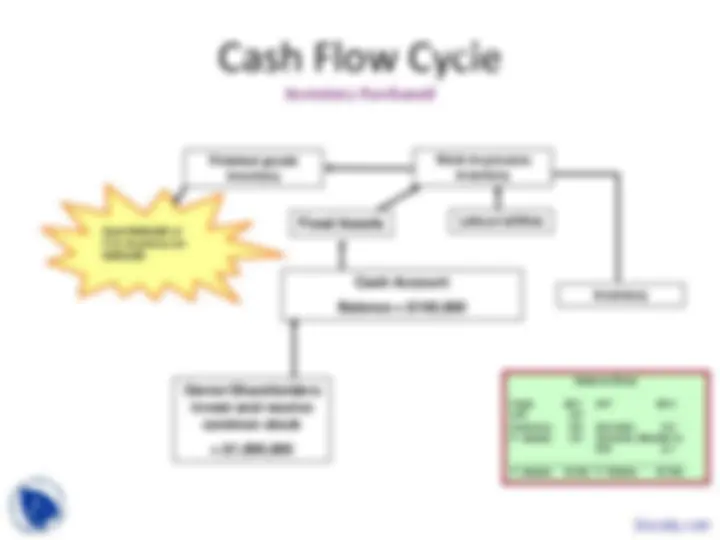

Cash Flow Cycle

Purchase of $500,000 Fixed Assets

Balance Sheet

Cash $0. F. Assets 0.5 Common Stock $1 m

T. Assets $1m T. Claims $1m

Cash Account

Balance = $500,

Owner/Shareholders

invest and receive

common stock

Fixed Assets

The firm purchases fixed

assets.

Step 3

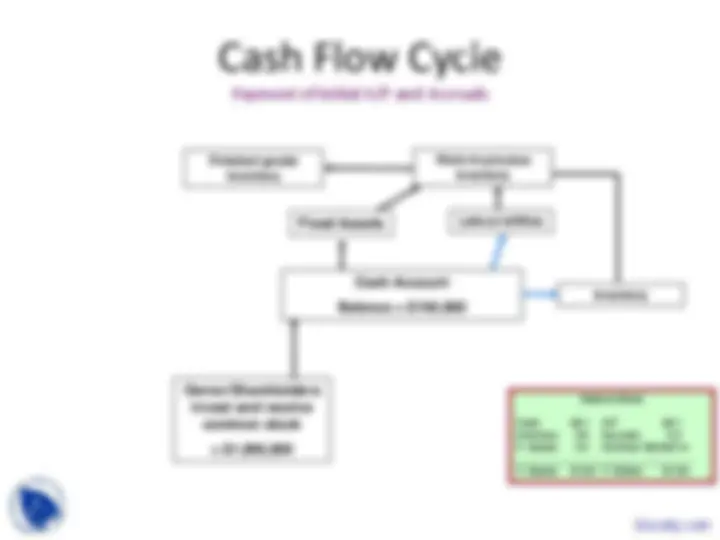

Cash Flow Cycle

Buy $300,000 of inventory on trade credit

Balance Sheet

Cash $0.5 A/P $0. Inventory 0. F. Assets 0.5 Common Stock $1 m

T. Assets $1.3m T. Claims $1.3m

Cash Account

Balance = $500,

Owner/Shareholders

invest and receive

common stock

Fixed Assets

Inventory

The firm purchases

$300,000 inventory from

suppliers. Step 4

Cash Flow Cycle

Payment of initial A/P and Accruals

Balance Sheet

Cash $0.1 A/P $0. Inventory 0.8 Accruals 0. F. Assets 0.4 Common Stock$1 m

T. Assets $1.3m T. Claims $1.3m

Cash Account

Balance = $100,

Owner/Shareholders

invest and receive

common stock

Fixed Assets

Inventory

Work-in-process

inventory

Labour/utilities

Depreciation

Finished goods

inventory

Labour and suppliers are

paid.

Step 6

Cash Flow Cycle

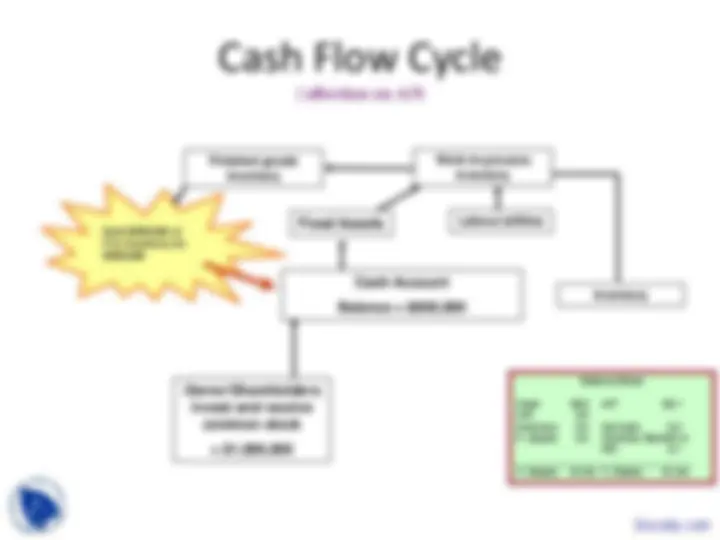

Goods sold on A/R for a profit

Balance Sheet

Cash $0.1 A/P $0. A/R 0. Inventory 0.4 Accruals 0. F. Assets 0.4 Common Stock$1 m R/E 0.

T. Assets $1.4m T. Claims $1.4m

Cash Account

Balance = $100,

Owner/Shareholders

invest and receive

common stock

Fixed Assets

Inventory

Work-in-process

inventory

Labour/utilities

Depreciation

Finished goods

inventory

Sold $400,000 of F.G. Inventory for $500,

Sale of inventory occurs.

Accounts receivable

created. Cash resources

near exhausted. 30 days

till A/R collected.

Step 7

Cash Flow Cycle

Value Added to W.I.P. Inventory

Balance Sheet

Cash $0.1 A/P $0. A/R 0. Inventory 1.2 Accruals 0. F. Assets 0.4 Common Stock$1 m R/E 0.

T. Assets $2.2m T. Claims $2.2m

Cash Account

Balance = $100,

Owner/Shareholders

invest and receive

common stock

Fixed Assets

Inventory

Work-in-process

inventory

Labour/utilities

Depreciation

Finished goods

inventory

Sold $400,000 of F.G. Inventory for $500,

Value is added to inventory

through labour ($300,000)

and equipment ($100,000). Step 9

Cash Flow Cycle

Suppliers and Employees Paid

Balance Sheet

Cash $0.1 A/P $0. A/R 0. Inventory 0.4 Accruals 0. F. Assets 0.4 Common Stock$1 m R/E 0.

T. Assets $1.4m T. Claims $1.4m

Cash Account

Balance = -$

Owner/Shareholders

invest and receive

common stock

Fixed Assets

Inventory

Work-in-process

inventory

Labour/utilities

Depreciation

Finished goods

inventory

Sold $400,000 of F.G. Inventory for $500,

Firm pays suppliers and

employees.

Step 10

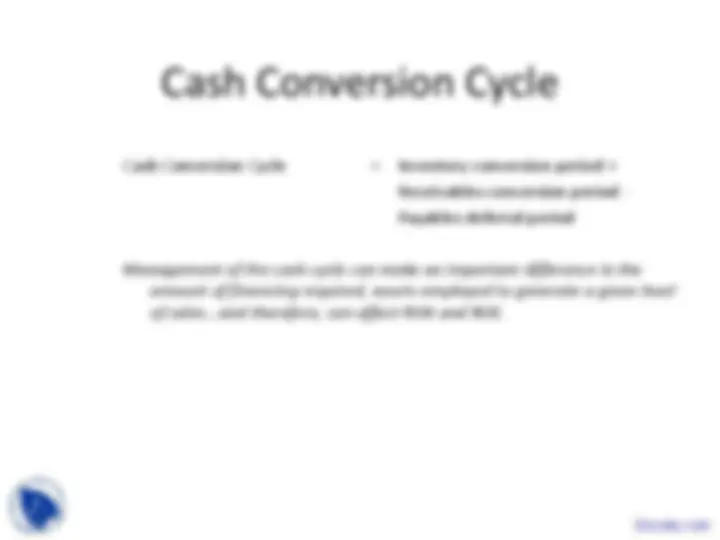

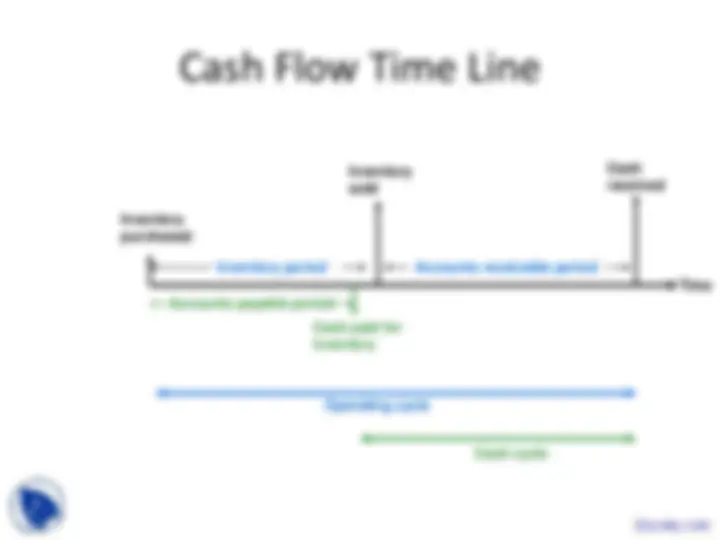

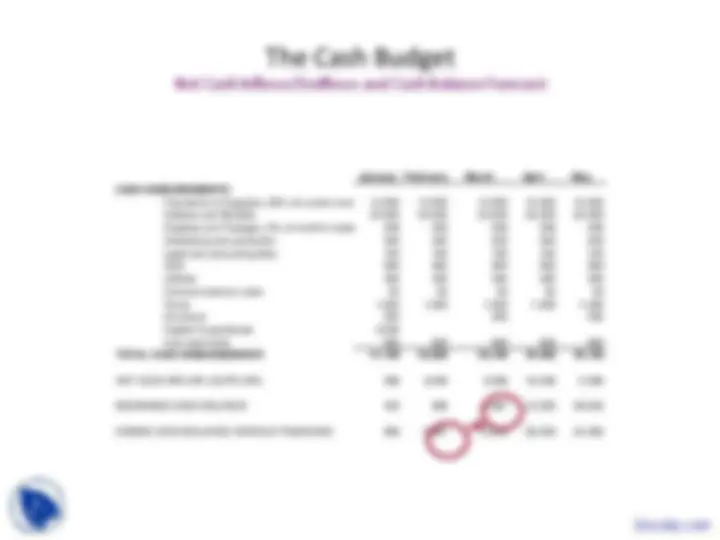

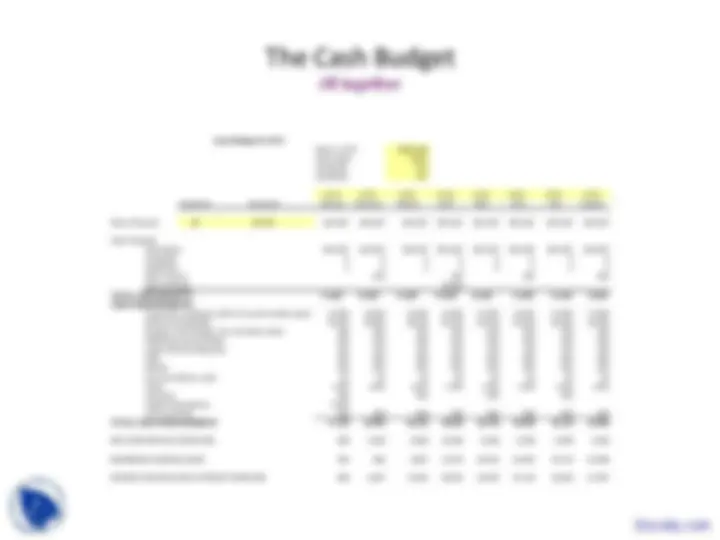

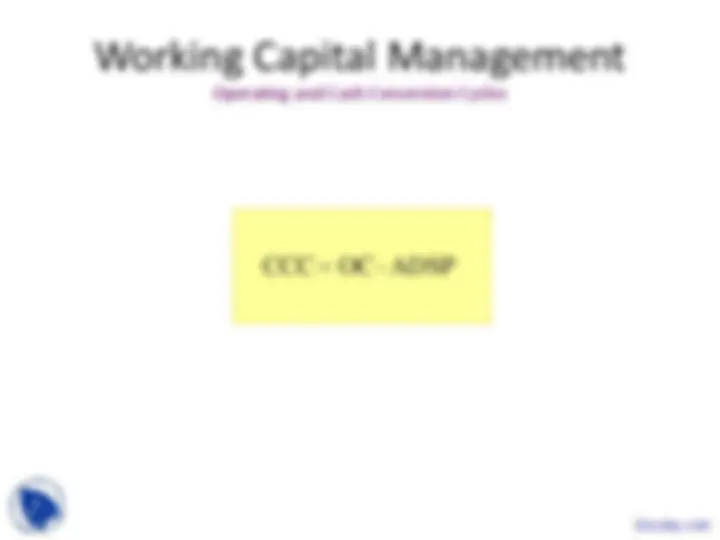

Cash Conversion Cycle

Cash Conversion Cycle = Inventory conversion period +

Receivables conversion period -

Payables deferral period

Management of the cash cycle can make an important difference in the

amount of financing required, assets employed to generate a given level

of sales...and therefore, can affect ROA and ROE.

Cash Flow Time Line

Inventory period

Inventory

sold

Cash

received

Inventory

purchased

Accounts receivable period

Operating cycle

Cash cycle

Cash paid for

inventory

Accounts payable period

Time