Payment of

Bonus Act,

1965

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Ppt on the Payment of Bonus Act, 1965

Typology: Lecture notes

1 / 25

This page cannot be seen from the preview

Don't miss anything!

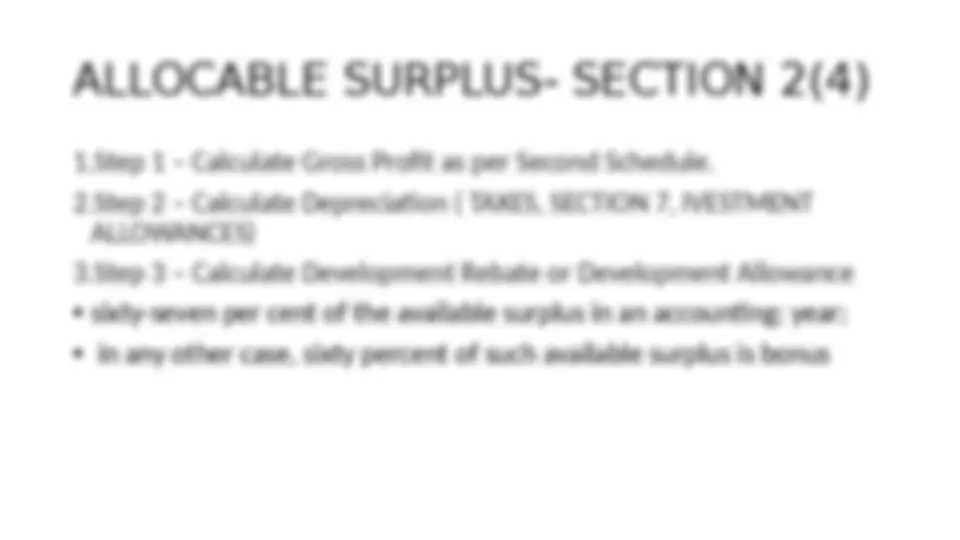

1.Step 1 – Calculate Gross Profit as per Second Schedule. 2.Step 2 – Calculate Depreciation ( TAXES, SECTION 7, IVESTMENT ALLOWANCES) 3.Step 3 – Calculate Development Rebate or Development Allowance