Linear Filter Model

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Linear Filter Model, Autoregressive Models, Moving Average Models, Autoregressive Moving Average, ARMA Filter, ARMA models, Parameters, Random disturbances, Substitute are points we learned in this lecture and you will find it interesting as well.

Typology: Slides

1 / 9

This page cannot be seen from the preview

Don't miss anything!

Time series in which successive values are highly dependent are regarded as generated from a series of independent shocks a (^) t. Shock are random, drawing from fixed distribution Normal, zero mean, variance σ a^2 the sequence of random variable at , a (^) t-1 , a (^) t-2 , …. is called white noise process

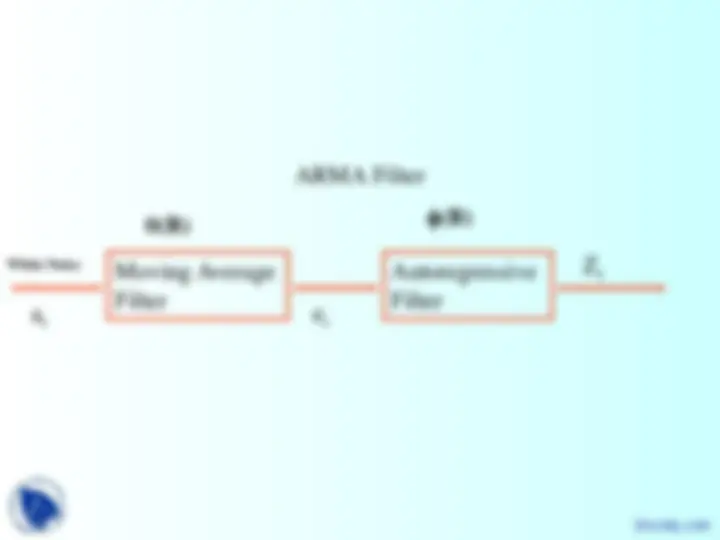

Linear Filter

White noise

a (^) t

Output z (^) t

ψ(B)

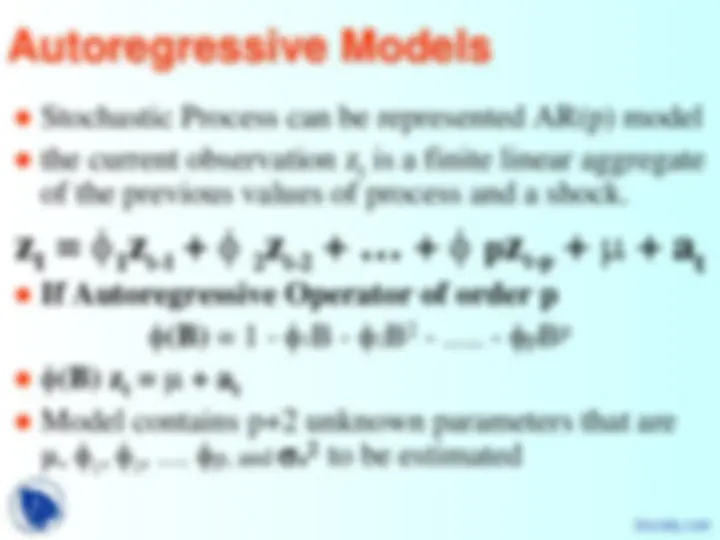

Stochastic Process can be represented AR(p) model the current observation zt is a finite linear aggregate of the previous values of process and a shock.

If Autoregressive Operator of order p φ (B) = 1 - φ1B - φ2B 2 - …. - φpB p φ (B) z (^) t = μ + a (^) t Model contains p+2 unknown parameters that are μ, φ 1 , φ 2 , … φp, and σ a^2 to be estimated

AR(p) process is special case of Linear Filter Substitute z (^) t-1 = φ 1 z (^) t-2 + φ (^) 2 z (^) t-3 + … + φ pz (^) t-p-1 + μ + a (^) t into AR(p) and so on φ (B) z (^) t = μ + a (^) t z (^) t - μ = φ (B)-1^ a (^) t z (^) t = μ + ψ(B) a (^) t So ψ(B) = φ (B)-

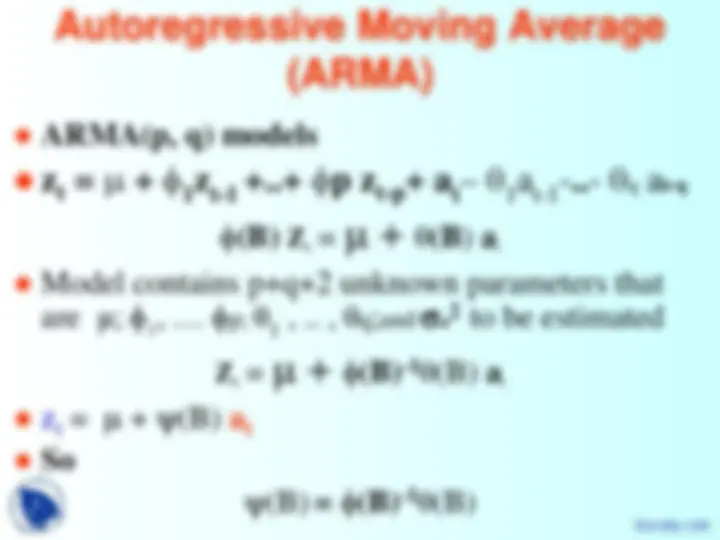

Model contains q+2 unknown parameters that are μ, θ 1 , θ 2 , … , θq and σ a^2 to be estimated z (^) t = μ + ψ(B) a (^) t So ψ(B) = θ(B)

ARMA(p, q) models

Model contains p+q+2 unknown parameters that are μ; φ 1 , … φp; θ 1 , .. , θq;and σ a^2 to be estimated

z (^) t = μ + ψ(B) a (^) t

So

ψ(B) = φ (B)-1 θ(B)