Lecture 14

Sergei Fedotov

20912 - Introduction to Financial Mathematics

Sergei Fedotov (University of Manchester) 20912 2010 1 / 7

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

A lecture note from the University of Manchester's 'Introduction to Financial Mathematics' course, focusing on delta hedging and the concept of Greek letters or Greeks in finance. The notes cover the calculation of delta for European call and put options, the use of put-call parity to find delta for European put options, and an introduction to the Greeks, which represent the sensitivities of options to changes in underlying parameters. The lecture also includes a delta-hedging example and problem sheet.

Typology: Summaries

1 / 22

This page cannot be seen from the preview

Don't miss anything!

Sergei Fedotov

20912 - Introduction to Financial Mathematics

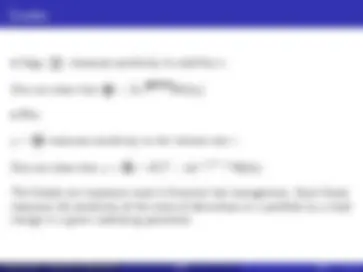

(^1) ∆-Hedging

(^2) Greek Letters or Greeks

Let us show that ∆ = ∂ ∂CS = N (d 1 ).

First, find the derivative ∆ = ∂ ∂CS by using the explicit solution for the European call C (S, t) = SN (d 1 ) − Ee−r^ (T^ −t)N (d 2 ).

Let us show that ∆ = ∂ ∂CS = N (d 1 ).

First, find the derivative ∆ = ∂ ∂CS by using the explicit solution for the European call C (S, t) = SN (d 1 ) − Ee−r^ (T^ −t)N (d 2 ).

= N (d 1 ) + SN′^ (d 1 )

∂d 1 ∂S − Ee−r^ (T^ −t)N′^ (d 2 )

∂d 2 ∂S

Find the value of ∆ of a 6-month European call option on a stock with a strike price equal to the current stock price ( t = 0). The interest rate is 6% p.a. The volatility σ = 0.16.

Find the value of ∆ of a 6-month European call option on a stock with a strike price equal to the current stock price ( t = 0). The interest rate is 6% p.a. The volatility σ = 0.16.

Solution: we have ∆ = N (d 1 ) , where d 1 = ln(S 0 /E )+(r +σ^2 / (^2) )T σ(T ) 12

Let us find Delta for European put option by using the put-call parity:

S + P − C = Ee−r^ (T^ −t).

Let us find Delta for European put option by using the put-call parity:

S + P − C = Ee−r^ (T^ −t).

Let us differentiate it with respect to S

Let us find Delta for European put option by using the put-call parity:

S + P − C = Ee−r^ (T^ −t).

Let us differentiate it with respect to S

We find 1 + ∂ ∂PS − ∂ ∂CS = 0.

Therefore ∂ ∂PS = ∂ ∂CS − 1 = N (d 1 ) − 1.

The option value: V = V (S, t | σ, r , T ).

Greeks represent the sensitivities of options to a change in underlying parameters on which the value of an option is dependent.

The option value: V = V (S, t | σ, r , T ).

Greeks represent the sensitivities of options to a change in underlying parameters on which the value of an option is dependent.

∆ = ∂ ∂VS measures the rate of change of option value with respect to changes in the underlying stock price

Γ = ∂ (^2) V ∂S^2 =^

∂∆ ∂S measures the rate of change in ∆ with respect to changes in the underlying stock price.

The option value: V = V (S, t | σ, r , T ).

Greeks represent the sensitivities of options to a change in underlying parameters on which the value of an option is dependent.

∆ = ∂ ∂VS measures the rate of change of option value with respect to changes in the underlying stock price

Γ = ∂ (^2) V ∂S^2 =^

∂∆ ∂S measures the rate of change in ∆ with respect to changes in the underlying stock price.

Problem Sheet 6: Γ = ∂ (^2) C ∂S^2 =^

N′(d 1 ) Sσ √ T −t ,^ where^ N

′(d 1 ) = √ 1 2 π e

− d

(^21) (^2).

One can show that ∂ ∂σC = S

T − tN′(d 1 ).

One can show that ∂ ∂σC = S

T − tN′(d 1 ).

ρ = ∂ ∂Vr measures sensitivity to the interest rate r.