Econometric Analysis of Panel Data

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Introduction to Econometrics, Theoretical foundations, Statistical foundations, Mathematical Elements, Model building, Inference, Semiparametric Regression, Data Structures are points which describes this lecture importance in Econometric Analysis of Panel Data course.

Typology: Slides

1 / 20

This page cannot be seen from the preview

Don't miss anything!

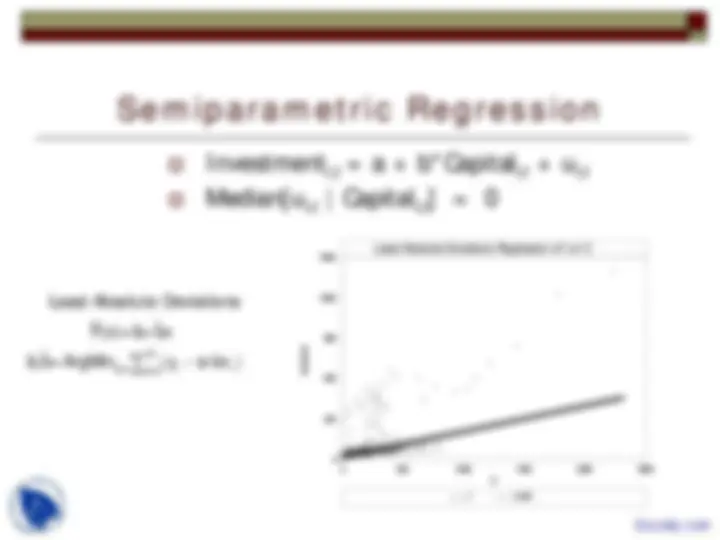

Nonparametric Regression of Investment on Capital Stock

KC

500

1000

1500

2000

0 0 500 1000 1500 2000 2500

Invstmnt

What are the assumptions?

What are the conclusions?

λ (^) λ

λ =

N

i=1 i i

N

i=1 i

i

.

Kernel Regression

w (z)y ˆ F(z)=

w (z)

1 x -z

( ) K

(t) (t)[1 (t)]

exp(t) (t)

1 exp(t)

i

i,t

i,t

i,t

i,t

i,t

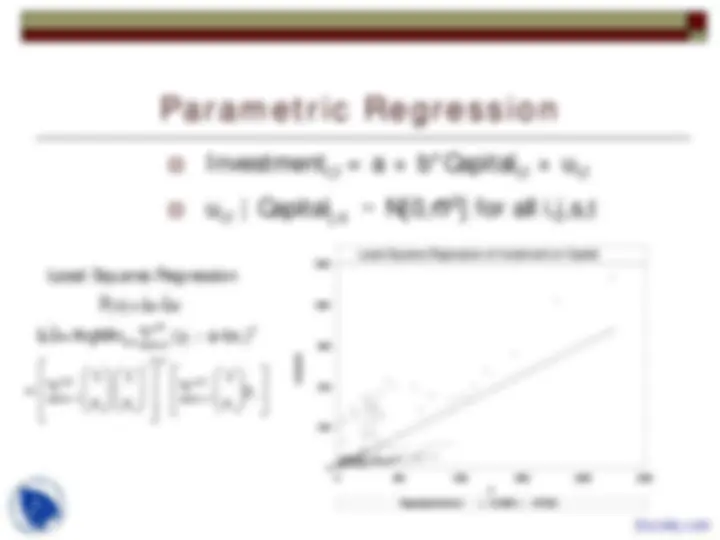

Least Absolute Deviations Regression of I on C

C

320

640

960

1280

1600

0 0 500 1000 1500 2000 2500

I ILAD

= (^) Invstmnt

− ∑

N

a,b (^) i 1 i i

Least Absolute Deviations

ˆ ˆ F(x)=a+bxˆ

ˆ ˆa,b=ArgMin |y a-bx |

Sharp, ‘exact’ inference about

only the sample – the ‘posterior’

density.