A New Rural

Finance Model

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

In the rural development we study the following concept:Eu Rural Development, New Council Regulation, Rural Development, Commission Implementing, Rules, Preparation, Delivery Structures, Programming and Reporting, Strategic Approach, Simplification

Typology: Slides

1 / 32

This page cannot be seen from the preview

Don't miss anything!

*Data as of 2004. World Bank estimates, using the ENIGH 2002.

Spacial Dispersion Covariance Risk

Ethnicity Issues Seasonality

No Integrated Prod. Chains

No Access to Financial Svcs.

Poverty

Migration

GOVT. BUDGET CONSTRAINTS

PRESENCE OF SUSTAINABLE FINANCIAL INSTITUTIONS

MARKET DEVELOPMENT

POLITICAL CONTEXT

MARKET FORCES ALONE WERE NOT ENOUGH TO ACHIEVE THE PUBLIC POLICY OBJECTIVE OF RURAL DEVELOPMENT

Development bank focused on agricultural activities

Funding through “unlimited” access to loans from the Federal Government

Operated as a subsity manager, with a high ratio of non- performing loans

Inefficient cost structure; operating costs over 100% of operating income

Defficient risk management

New Development Agency focused on rural productive projects

Legally banned from taking deposits, loans or market funding. Must maintain endowment value over time to sustain operations

Operates with credit processes that apply international best practices. Has spread payment culture among clients

Efficient cost structure

Best risk management practices

Banrural (^) Financiera Rural

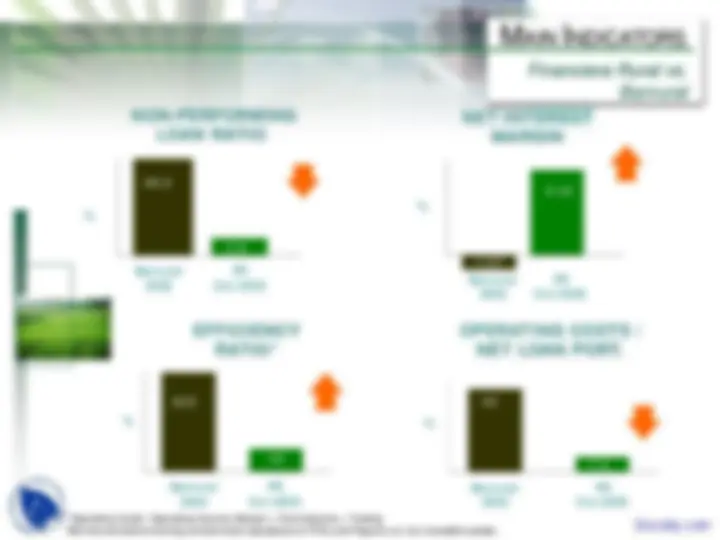

C OMPARATIVE A NALYSIS

Financiera Rural vs. Banrural

[1] Even thouth currently Financiera Rural operates in the first tier, as well as the second, in the long term it expects to serve only as a second-tier lending institution.

RURAL DEVELOPMENT AGENCY

Initial Endowment of USD 1.72 billion** USD 1,534 Mill. Credit*

USD 79 Mill. pre-operating expenses

USD 49 Mill. Technical Assistance

Supervised Rural Financial Intermediaries

Informal Rural Credit Institutions

Individual Rural Producers

Technical assistance for credit enhancement and the creation of RFIs

Credit

*Of the initial USD 1.6 billion, USD 46 million could be used for the acquisition of Banrural assets (other than loans). ** Provided by Congress.

Rural Financial Intermediaries

*Governed by the new law for popular savings and loans ( Ley de Ahorro y Crédito Popular )

Other Organizations

Conception of the Project

Commercialization Of the Product

Before Granting Credit

Specialized Technical Assistance and Training

Establishment

Sustainable Development

Individual Producers

Unsupervised Credit Organizations

Supervised Rural Financial A (^) Intermediaries Z

FR’s Credit and Technical Assistance to Develop Institutional Capabilities