Macroeconomics VIII:

Equilibrium of Aggregate Supply

and Demand

Gavin Cameron

Lady Margaret Hall

Hilary Term 2004

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

An excerpt from a university lecture note written by Gavin Cameron during Hilary Term 2004 at Lady Margaret Hall. It covers the topics of aggregate demand, the aggregate demand curve, long-run and short-run aggregate supply, and the impact of shocks on the economy. the determinants of aggregate demand, the reasons why the aggregate demand curve slopes downwards, and the concept of equilibrium output in the long and short run. It also discusses the role of fiscal and monetary policy in managing economic fluctuations.

What you will learn

Typology: Slides

1 / 18

This page cannot be seen from the preview

Don't miss anything!

aggregate demand revisited•^

Aggregate demand comprises four components:•

consumption

-^

investment

-^

primary government spending (i.e. net of transfers)

-^

net exports

The level of income (both current and expected) is a majordeterminant of consumption, government spending and net exports.

-^

The real exchange rate is a major influence on net exports.

-^

The interest rate is also an influence on consumption and investment(with the latter being also dependent upon output expectations and‘animal spirits’).

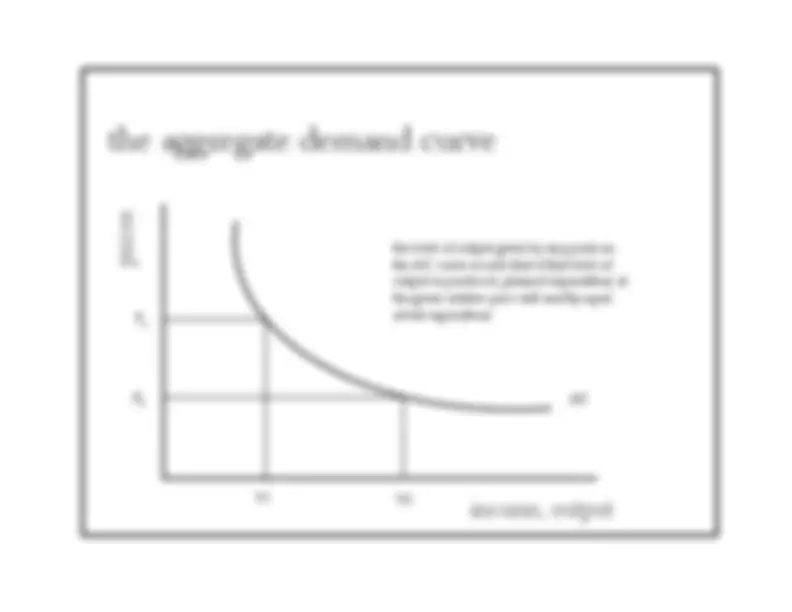

the aggregate demand curve

P^1 P^0

the level of output given by any point onthe AD curve is such that if that level ofoutput is produced, planned expenditure atthe given relative price will exactly equalactual expenditure

AD

Y

Y

long-run aggregate supply revisited•^

-^

-^

-^

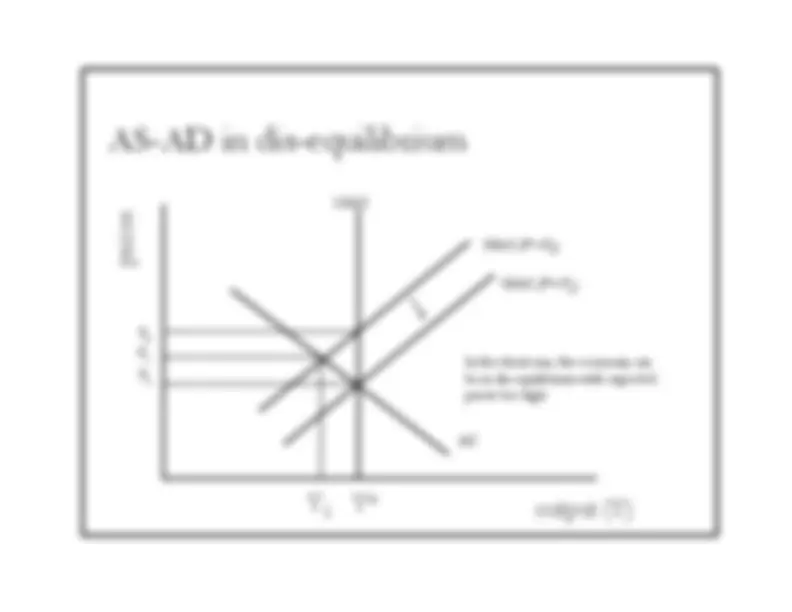

AS-AD in long-run equilibrium

LRAS

SRAS

(P^1

e^ =P

) 1

P^1

AD

1

AS-AD in dis-equilibrium

LRAS

SRAS (P

e =P

) 0

P^2

AD

P^0 P^1

1

In the short-run, the economy canbe in dis-equilibrium with expectedprices too high

SRAS (P

e =P

)^2

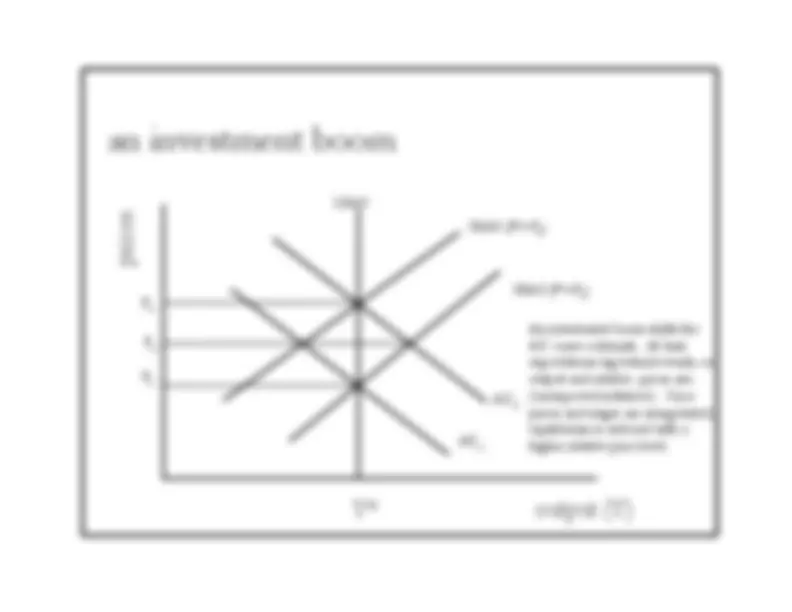

an investment boom

LRAS

SRAS (P

e =P

) 1

P^1

AD

1

AD

2

SRAS (P

e =P

)^3

P^3 P^2

An investment boom shifts theAD curve outwards. At first,expectations lag behind events, sooutput and relative prices rise(‘unexpected inflation’). Onceprices and wages are renegotiated,equilibrium is restored with ahigher relative price level.

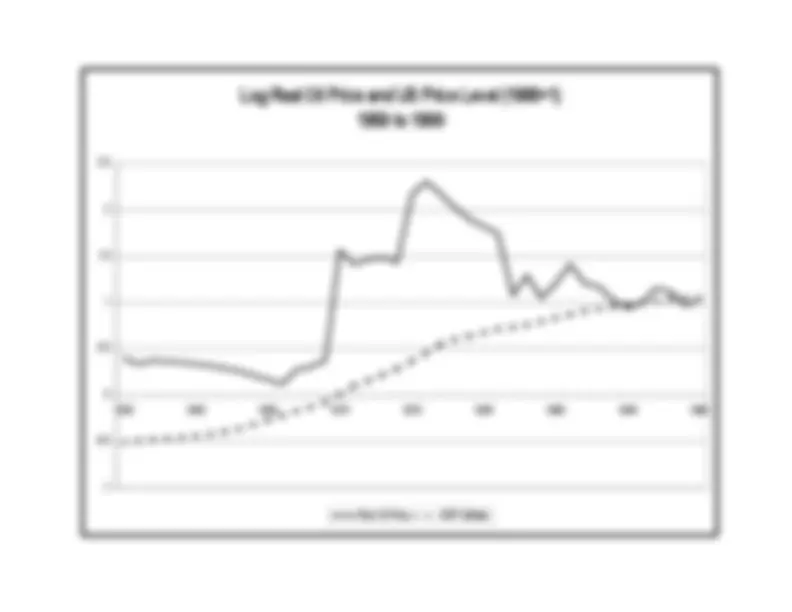

an ‘oil price shock’ & labourreal wage

1

1

W^1

/P

1 W^2

/P

2

2

LS LD

2

Labour productivity falls since production has toswitch to less energy-intensive techniques.Hence, the marginal product of labour falls anddemand for labour shifts inwards. Theequilibrium real wage and employment falls

Log Real Oil Price and US Price Level (1995=1)

1959 to 1999

2.5^2 1.5^1 0.5^01959 -0.5^ -

1964

1969

1974

1979

1984

1989

1994

1999

Real Oil Price

GDP Deflator

fiscal policy•^

‘If the Treasury were to fill old bottles with bank notes, bury them atsuitable depths in disused coal mines which are then filled up withtown rubbish, and leave them to private enterprise… to dig them upagain, there need be no more unemployment. It would, indeed, bemore sensible to build houses and the like, but if there are political andpractical difficulties in the way of this, the above would be better thannothing’ J.M. Keynes, 1936.

-^

Changes in the government’s fiscal stance (that is, the differencebetween government spending and taxation) will shift the aggregatedemand curve.

-^

If economy is at equilibrium output, increases in spending (or tax cuts)will lead to an inflationary boom, which eventually will lead only tohigher prices.

-^

If economy is below equilibrium output, increases in spending (or taxcuts) will tend to raise output (as well as prices) and shift the economyback to equilibrium.

monetary policy•^

‘Having regard to human nature and our institutions, it can only be afoolish person who would prefer a flexible wage policy to a flexiblemoney policy, unless he can point to advantages from the former thatare not obtainable from the latter’ J.M.Keynes, 1936.

-^

Monetary policy can be implemented through either changes in themoney supply or interest rate. A cut in the interest rate leads to a risein the money supply.

-^

Changes in the interest rate will shift the aggregate demand curve.

-^

If economy is at equilibrium output, interest rate cuts will lead to aninflationary boom, which eventually will lead only to higher prices.

-^

If economy is below equilibrium output, interest rate cuts will tend toraise output (as well as prices) and shift the economy back towardsequilibrium.

the theory of short-run fluctuations

Keynesian CrossMoney Market

IS Curve LM Curve

IS-LM model

AD curve AS curve

AS-AD model