Capital

markets

day

27th September 2017

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

European airline market based on total short haul capacity ... Currently critical for FSC strategies and therefore likely to endure.

Typology: Study notes

1 / 90

This page cannot be seen from the preview

Don't miss anything!

Agenda

Time Agenda item Led by 11.00 Introduction Carolyn McCall 11.05 1. Market / Network

Airline industry trends A winning network strategy Q&A

Robert Carey Andrew Hodges

11.45 2. Driving Revenue Peter Duffy James Millett Andrew Middleton Lis Blair 12:30 LUNCH 13.30 3. easyJet cost control & a strong balance sheet easyJet’s cost position

easyJet LEAN Airports and ground handling Strong balance sheet Q&A

Andrew Findlay Paul Ablin Simon Cox Mike Hirst

14.30 4. Making travel easy & affordable

The easyJet operation / avoiding disruption Digital operations Gatwick Airport Q&A

Chris Browne Gary Smith Chris Hope

15.15 Wrap up and close Carolyn McCall

15:30 Gatwick North Terminal tour / Innovation presentation

Chris Hope

17:30 End of day

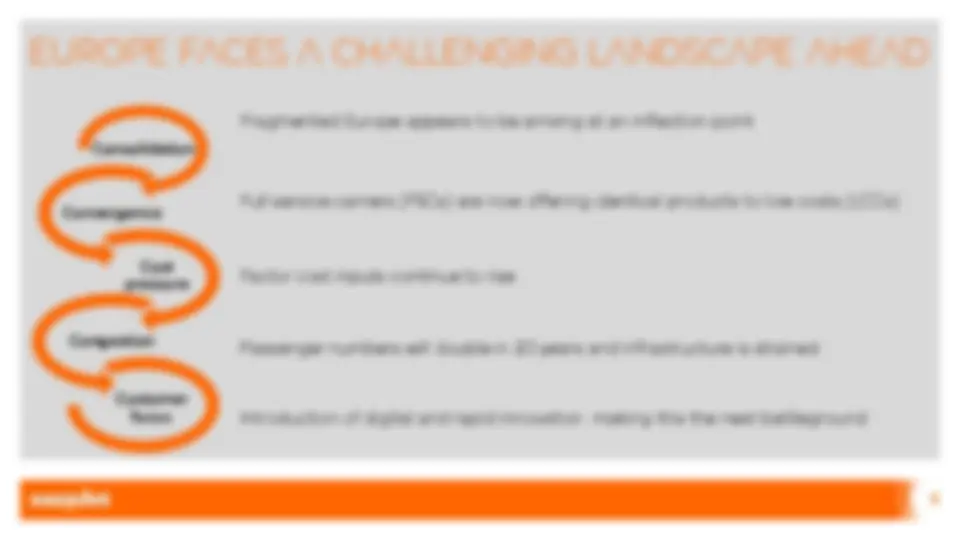

Europe faces A challenging landscape ahead

Fragmented Europe appears to be arriving at an inflection point

Full service carriers (FSCs) are now offering identical products to low costs (LCCs)

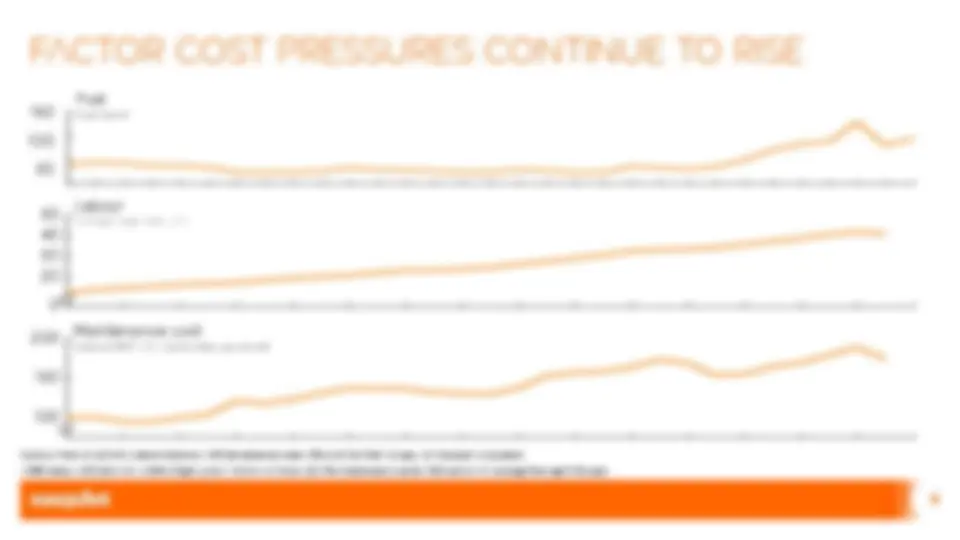

Factor cost inputs continue to rise

Introduction of digital and rapid innovation making this the next battleground

Passenger numbers will double in 20 years and infrastructure is strained

Charge for reserved seating

Charge for on-board food offering

Charge for hold baggage

Flexi fares

Charge for reserved seating

Charge for on-board food offering

Charge for hold baggage

Flexi fares

Airline business models are converging

Traditional advantages

of a Hub feeder

model are eroding

passenger volumes and associated

congestion is growing

Source: IATA 20 year passenger forecast

7,200,000,

Number of passengers predicted by 2035, ~2x today’s volume

Growth in the UK

Growth in France

Growth in Spain

Growth in Germany

Growth in Italy

Looking at Easyjet Markets by 2035…

+50%

+50%

+40%

+35%

+30%

INDUSTRY

Integrated loyalty and data with hotel, shared ride

Creates buzz around its brand during holidays and special occasions

Opaque pricing model that creates bundles of multiple trips

Self-serve mobile rebooking in case of delays/ cancellations

Redesigned airport experience (e.g. pre order coffee pickup)

Allows passengers order food and drinks through its IFE

Allows customers to track the status and location of baggage in real

Data and digital are driving a new focus on Customer

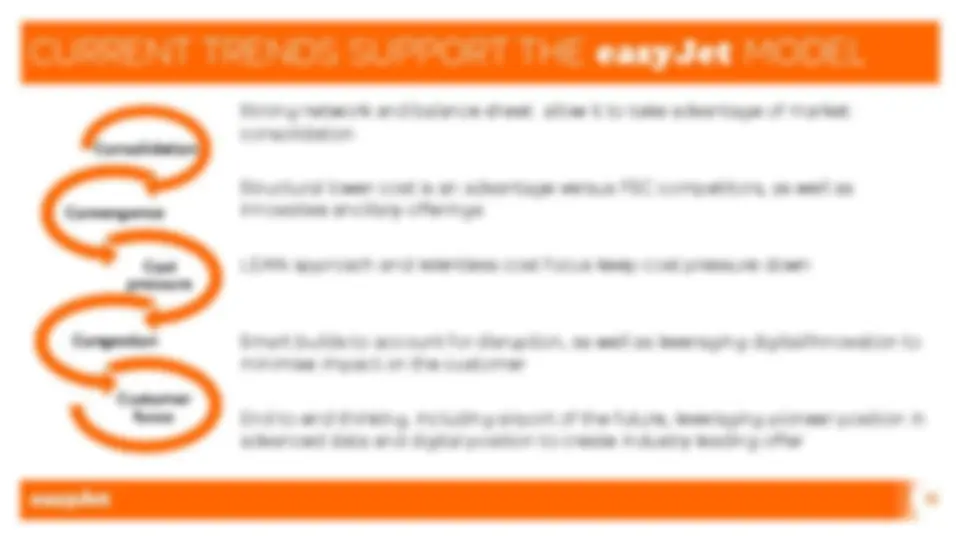

current trends support THE easyJet model

Strong network and balance sheet allow it to take advantage of market consolidation

Structural lower cost is an advantage versus FSC competitors, as well as innovative ancillary offerings

LEAN approach and relentless cost focus keep cost pressure down

End to end thinking, including airport of the future, leveraging pioneer position in advanced data and digital position to create industry leading offer

Smart builds to account for disruption, as well as leveraging digital/innovation to minimise impact on the customer

The easyJet Network

#1 positions deliver sustainable returns

Strong correlation between strong performance and #1 positions and constrained airports

We have a targeted plan to build more airports into # positions and to secure slots at constrained airports

Superior product

widest range of routes

best frequencies / times

strongest brand awareness

Cost advantage

negotiated airport fees

procurement of ground handling

economies of scale from media spend

Operational advantage

improved crew productivity

more flexible scheduling (larger slot portfolio)

#1 positions

Constrained, not #1 Neither constrained nor #

Returns

Strong progress over last five years

2013 2017

Airports in #1/2 positions 44 47

Market share at #1/2 positions 24% 26%

Capacity at #1/2 positions (m) 52.5 64.

138 airports europe

(^28) bases

31 countries 874 routes

279 aircraft

over 86

m seats p.a.

FY

easyJet capacity split by airport position, FY 98% of seats are on routes that touch a #1 or #2 position

easyJet Legacies Other LCCs

easyJet Legacies

Significant scope for further profitable growth

Over the next 3 years our fleet will grow by around 40 aircraft

On existing routes alone there remains significant scope to grow through:

We have a c.9% share of the total European market - new route opportunities support further significant profitable growth

easyJet Routes FY17 capacity (m)

Equivalent to 371 easyJet aircraft

easyJet Routes FY17 capacity (m)

Equivalent to 183 easyJet aircraft

Targeted investment to create

winning competitive positions

Growth balanced between strengthening

current positions and seeding new opportunities

This will create 5 - 10 additional #1 positions

We will continue to take share and grow

market positions by competing with inefficient legacy carriers

Indicative allocation of growth to FY

Maintain existing # positions Achieve # position - current bases

Seed new #1/ positions