Econometric Analysis of Panel Data

21. Bayesian Econometric Models

for Panel Data

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Bayesian Econometric Models, Panel Data, Philosophical Underpinning, Objectivity and Subjectivity, Paradigms, Applications of the Paradigm, Likelihoods, Likelihood Principle are points which describes this lecture importance in Econometric Analysis of Panel Data course.

Typology: Slides

1 / 56

This page cannot be seen from the preview

Don't miss anything!

21. Bayesian Econometric Models

for Panel Data

A Philosophical Underpinning

Paradigms

Evidence consistent with theory? Theory stands and waits for

more evidence to be gathered

Evidence conflicts with theory? Theory falls

Applications of the Paradigm

The Likelihood Principle

Application:

th

7 13

7 13

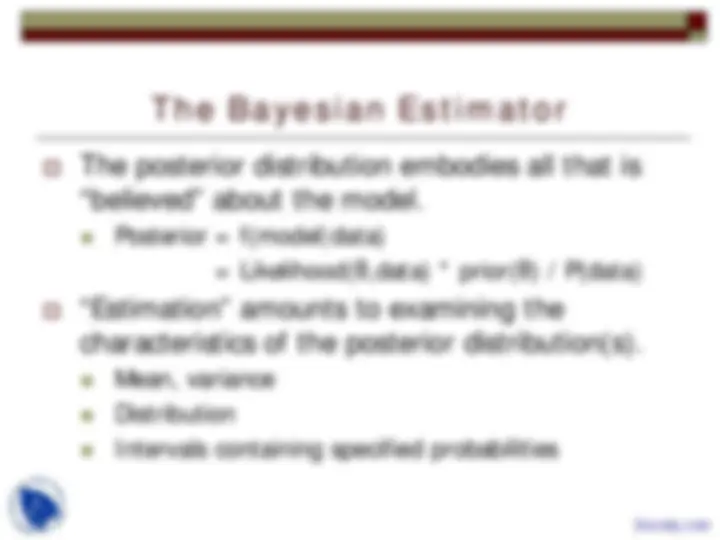

The Bayesian Estimator

Priors and Posteriors

Conjugate Prior

s N s s N s

a 1 b 1

Mathematical device to produce a tractable posterior

This is a typical application

N (^) (N 1) L( ;N,s)= (1 ) (1 )

s (s 1) (N s 1)

(a+b) Use a , p( )= (1 )

(a) (b)

Po

− −

− −

Γ + θ (^) θ − θ = θ − θ

Γ^ +^ Γ^ −^ +

Γ θ θ − θ Γ Γ

conjugate beta prior

s N s a 1 b 1

1 s N s a 1 b 1

0

s a 1 N s b 1

1 s a 1 N s b

0

(N 2) (a+b) (1 ) (1 ) (s 1) (N s 1) (a) (b) sterior (N 2) (a+b) (1 ) (1 ) d (s 1) (N s 1) (a) (b)

(1 )

(1 )

− − −

− − −

− − + −

− − + −

Γ + Γ θ^ − θ^ θ^ − θ Γ^ +^ Γ^ −^ +^ Γ^ Γ = Γ + Γ θ^ − θ^ θ^ − θ^ θ Γ^ +^ Γ^ −^ +^ Γ^ Γ

θ − θ

1

a Beta distribution.

d

s+a Posterior mean = (we used a = b = 1 before)

N+a+b

=

θ

Bayesian Estimators

= ∫

f(data | )p( ) E( | data) d β f(data)

β β β β β

Marginal Posterior for β

2

2 2 / 2 1 / 2

2 1 / 2 2

2 1

After integrating out of the joint posterior:

[ ] ( / 2) [2 ] | | ( 2) ( | , ). [ ( ) ( )]

n-K

Multivariate t with mean and variance matrix [ ( ) ]

2

The Bayesi

v K

d K

ds d K

d f

ds

s n K

σ

π

− −

−

Γ + ′

Γ + ∝

− −

X X

β y X β b X X β b

b X'X

an 'estimator' equals the MLE. Of course; the prior was

noninformative. The only information available is in the likelihood.

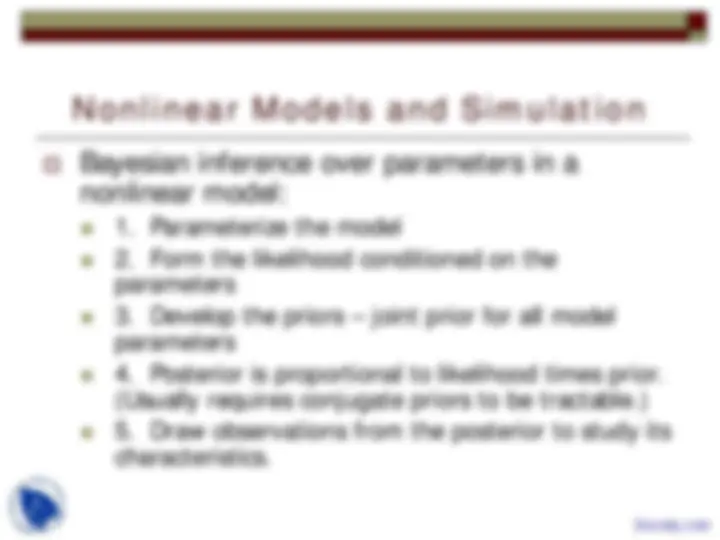

Nonlinear Models and Simulation